For many veterans, the VA loan program is a cornerstone of achieving homeownership. But a common question often arises: can I use my VA loan to buy land? Understanding the limitations, eligibility requirements, and alternative options is critical for veterans exploring land purchases. In this guide, we break down the facts, offer practical advice, and explain how VA loans can help you secure your dream property.

Understanding VA Loans

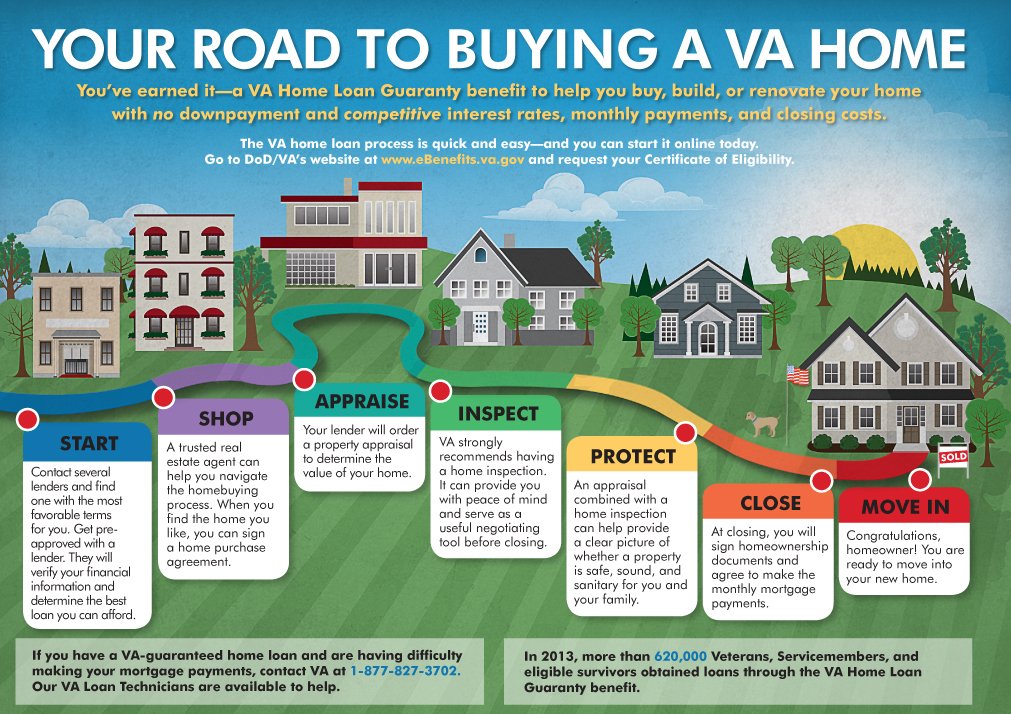

A VA loan is a mortgage program backed by the U.S. Department of Veterans Affairs, designed to help eligible veterans, active-duty service members, and certain members of the National Guard and Reserves purchase homes. Some of the key benefits of VA loans include:

- No down payment required (in most cases)

- No private mortgage insurance (PMI)

- Competitive interest rates

- Flexible credit requirements

The VA guarantees a portion of the loan, which reduces the risk to lenders and allows for these favorable terms.

Can I Use My VA Loan to Buy Land?

The short answer is generally no. VA loans are intended to finance primary residences, meaning the property must include a habitable dwelling that the veteran will occupy. Raw, undeveloped land by itself is not eligible for VA financing.

However, there are ways a VA loan can be applied to land purchases in specific situations:

- Land with Construction Plans – VA loans can be used for a construction-to-permanent loan where the land and home are financed together.

- Existing Home on Land – If the land already has a home on it, you can purchase it using a standard VA loan.

- Hybrid Loans – Some VA-approved lenders offer specialized loans for land purchase combined with construction.

How VA Construction Loans Work

A VA construction loan allows veterans to buy land and build a home, effectively enabling land ownership through VA benefits. Here’s how it works:

| Feature | Details |

|---|---|

| Loan Type | Construction-to-permanent VA loan |

| Purpose | Purchase land and finance construction of a primary residence |

| Occupancy | Must live in the home upon completion |

| Down Payment | Typically no down payment if VA entitlement covers costs |

| Lender Requirement | Must work with VA-approved lender and builder |

| Funds Disbursement | Released in stages during construction |

| Conversion | Converts to standard VA mortgage after construction completion |

Steps to Use Your VA Loan for Land and Construction

If you want to buy land using your VA loan, follow these steps:

- Confirm VA Eligibility – Check your VA entitlement to ensure sufficient coverage for land and construction costs.

- Select a VA-Approved Lender – Not all lenders offer construction loans, so choose one experienced with VA construction financing.

- Find a VA-Approved Builder – The VA requires builders to meet specific standards to protect veterans.

- Secure Land and Construction Plans – Prepare blueprints, cost estimates, and permits for lender approval.

- Apply for a VA Construction Loan – Submit your application with financial documentation and construction plans.

- Draw Funds During Construction – Lenders release money in stages tied to inspections.

- Convert to Permanent VA Mortgage – Once construction is complete, the loan transitions to a permanent VA loan with standard terms.

Advantages of Using a VA Loan for Land

- No Down Payment – Many veterans can buy land and build a home without paying a down payment.

- Single Loan Convenience – Construction-to-permanent VA loans consolidate land and home financing into one process.

- Custom Home Opportunity – Veterans can design homes that meet their specific needs on the land they purchase.

- VA Guarantees – The VA backing reduces lender risk, often leading to lower interest rates.

Limitations and Considerations

- Not for Raw Land Alone – You cannot use a VA loan to buy undeveloped land without a home plan.

- Occupancy Requirement – The VA requires the property to be your primary residence.

- Entitlement Usage – Buying land and constructing a home may use a significant portion of your VA entitlement.

- Approval Complexity – VA construction loans are more complex than standard VA loans, requiring detailed plans and inspections.

Table: VA Loan Eligibility for Land Scenarios

| Property Type | VA Loan Eligible? | Notes |

|---|---|---|

| Raw Land | No | VA loans do not cover vacant land without plans for a home |

| Land + Home Construction | Yes | Must use construction-to-permanent VA loan |

| Existing Home on Land | Yes | Standard VA loan can be used |

| Investment Land or Property | No | VA loans cannot finance rental or investment land |

| Manufactured Home on Land | Yes | Must meet VA standards and primary residence requirement |

FAQs About Using a VA Loan for Land

Q1: Can I use my VA loan to buy acreage?

Yes, but only if there is a home on the property or you are using a VA construction loan to build a home.

Q2: What is a VA construction-to-permanent loan?

It’s a VA-backed loan that finances land purchase and home construction, converting to a standard mortgage once construction is finished.

Q3: Can I use my VA loan to buy land for investment purposes?

No, VA loans are strictly for primary residences, not investment properties.

Q4: Do I need a down payment to buy land with a VA loan?

If your VA entitlement covers the total cost, usually no down payment is required.

Q5: How do I find a VA-approved builder?

Your VA-approved lender can provide a list of builders that meet VA construction standards.

Q6: Can I buy land and build a custom home using my remaining VA entitlement?

Yes, as long as your remaining entitlement is sufficient for the total loan amount.

Q7: How long does it take to approve a VA construction loan?

Approval can take longer than standard VA loans due to construction plan reviews and inspections, often several weeks or months.

Q8: What if construction costs exceed the initial estimate?

You may need additional financing or an adjusted loan amount approved by your lender, within VA entitlement limits.

Key Considerations Before Buying Land With a VA Loan

- Remaining VA Entitlement – Make sure you have enough VA entitlement to cover land and construction.

- Builder Selection – Choose a reliable, VA-approved builder with experience in construction loans.

- Financial Planning – Include contingency funds for construction overruns.

- Local Regulations – Check zoning, permits, and land use restrictions before purchasing.

- Lender Requirements – Each lender may have additional requirements for construction loans.

Conclusion

While a VA loan cannot typically be used to purchase raw land alone, it is possible to buy land and build a home using a VA construction-to-permanent loan. Understanding your VA entitlement, the occupancy requirements, and the construction loan process is essential to leveraging your VA benefits effectively. With proper planning and guidance from VA-approved lenders and builders, veterans can achieve the dream of land ownership and a custom home.