7 Key Truths About Home Equity Loan Interest Rates in 2026

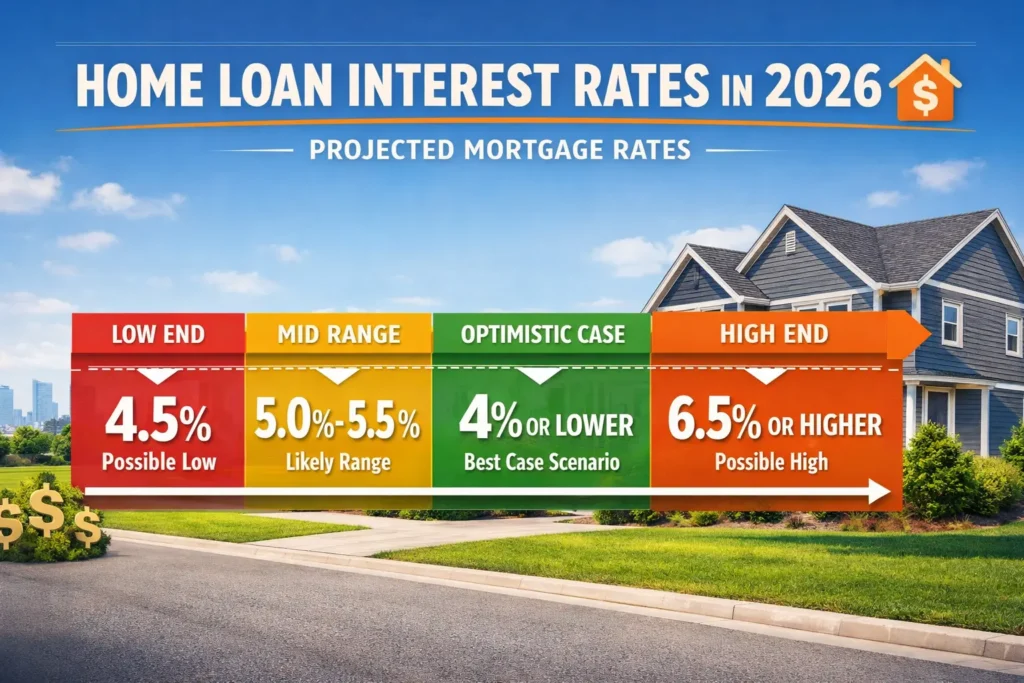

The spring of 2026 has brought a new sense of clarity to the housing market. After years of economic recalibration, homeowners are sitting on record-breaking levels of equity. Whether you are looking to consolidate high-interest debt or finally pull the trigger on that modern kitchen remodel, understanding home equity loan interest rates is the first step toward making a sound financial decision. I’ve seen a distinct shift in how people approach borrowing. It’s no longer just about the “lowest number”—it’s about the total cost of capital over time. In this comprehensive guide, we will break down the current landscape of home equity loan interest rates, how they differ from other products, and how you can optimize your financial profile to secure the best deal possible. 1. The 2026 Rate Snapshot: Where We Stand Today As of April 28, 2026, home equity loan interest rates have reached a plateau. The national average for a 15-year fixed-rate home equity loan is currently hovering around 7.91% to 8.03%. This represents a significant stabilization compared to the volatility of 2024 and 2025. While these home equity loan interest rates are higher than the historic lows of a few years ago, they remain much more attractive than unsecured borrowing. For comparison, the average credit card interest rate in 2026 is still well above 22%. By utilizing home equity loan interest rates, you are effectively trading high-interest debt for a more manageable, fixed-rate installment plan. 2. Fixed vs. Variable: Choosing Your Strategy When researching home equity loan interest rates, it is vital to distinguish between a standard home equity loan and a Home Equity Line of Credit (HELOC). In the current economic climate, many homeowners are choosing the security of fixed home equity loan interest rates to protect themselves against any future inflationary spikes. Comparison: Fixed Home Equity Loans vs. HELOCs (April 2026) Feature Home Equity Loan HELOC Current Avg. Rate 7.91% (Fixed) 7.09% (Variable) Rate Stability Guaranteed for the life of the loan Fluctuates with the Market Payout Lump Sum Draw as needed Best For… One-time major expenses Ongoing projects or emergencies Export to Sheets 3. How Lenders Calculate Your Specific Rate Not everyone receives the same home equity loan interest rates. Lenders use a “risk-based pricing” model. To get the best home equity loan interest rates, you need to optimize three key metrics: +1 4. The Impact of Geopolitics on Your Wallet Why are home equity loan interest rates sitting at 8% instead of 5%? In 2026, global stability plays a massive role. The ongoing tensions in the Middle East have kept energy prices elevated, which in turn keeps the Federal Reserve cautious about cutting the benchmark rates that influence home equity loan interest rates. As long as the Fed maintains a “higher for longer” stance to ensure inflation remains at the 2% target, home equity loan interest rates are expected to stay within the 7.5% to 8.5% corridor for the remainder of the year. 5. Regional Variations: Why Location Matters While we discuss national averages, home equity loan interest rates can vary significantly by state. Credit unions and community banks in the Midwest often offer home equity loan interest rates that are 0.25% to 0.50% lower than national commercial banks. Always check with a local institution before signing. Sometimes, a smaller bank’s desire to grow their local portfolio can lead to highly competitive home equity loan interest rates that you won’t find on a national search engine. 6. The Tax-Deductibility Factor A major advantage of home equity loan interest rates is the potential tax benefit. According to current 2026 tax laws, the interest paid on a home equity loan is generally deductible if the funds are used to “buy, build, or substantially improve” the home that secures the loan. This effectively lowers your “real” home equity loan interest rates once you factor in your tax savings. 7. How to Spot the Best Offers Lenders often use teaser home equity loan interest rates to capture search traffic. When you land on a page, look for the “Disclosure” or “Terms” link. The real home equity loan interest rates you’ll pay are often 1% to 2% higher than the headline if you have a credit score under 740. True authority in a lender comes from transparency—if they hide their home equity loan interest rates calculator, they might be hiding higher fees too. Frequently Asked Questions (FAQs) What are the current home equity loan interest rates for April 2026? The national average is approximately 7.91% for a 5-year term and 8.03% for a 15-year term. Is it better to get a personal loan or a home equity loan? Home equity loans generally offer much lower interest rates than personal loans because they are secured by your home. However, personal loans are faster to close and don’t put your property at risk. Will home equity loan interest rates go down in 2027? Most analysts predict that home equity loan interest rates will only see significant decreases if the Federal Reserve feels confident that inflation has been permanently defeated. Current forecasts suggest a very slow decline starting in mid-2027. How much equity do I need to qualify? Most lenders require you to keep at least 15% to 20% equity in your home after the loan is taken out. Can I get fixed home equity loan interest rates for 30 years? While 10-year and 15-year terms are the most common, some specialized lenders do offer 20-year and 30-year fixed home equity loan interest rates, though they typically come with a slight rate premium. Final Thoughts for 2026 Homeowners Navigmortgagerefinancerates.comating mortgagerefinancerates.com requires a balance of market knowledge and personal financial discipline. While the rates today aren’t the “free money” of the past decade, they represent a stable and useful tool for building long-term wealth through home improvement or strategic debt management. Don’t be afraid to shop around. A difference of just 0.5% in home equity loan interest rates can save you thousands of dollars over the life of the loan.

6 Essential Insights into the PNC Home Equity Loan Experience in 2026

When you’ve spent years building equity in your property, there comes a point where you want that value to start working for you. In the current financial landscape of April 2026, homeowners are increasingly looking at the PNC home equity loan as a strategic way to fund major life goals. Whether you’re planning a sustainable home retrofit or consolidating debt following the recent economic shifts, understanding how this specific lender operates is key. I’ve noticed a significant uptick in people searching for “stability” in their borrowing. PNC Bank has positioned itself as a titan in this space, offering products that cater to those who prefer the predictability of fixed payments. In this comprehensive guide, we’ll dive deep into the mechanics of the PNC home equity loan, compare it to other market options, and help you determine if it’s the right vehicle for your financial journey. 1. What Exactly is the PNC Home Equity Loan? At its core, the PNC home equity loan—often categorized by the bank as a Home Equity Installment Loan—is a second mortgage that provides you with a one-time lump sum of cash. Unlike a line of credit that you draw from over time, this loan gives you the full amount upfront, which you then repay over a set term at a fixed interest rate. In 2026, PNC remains one of the few national lenders that still champions the traditional installment structure alongside its more flexible HELOC products. This is particularly appealing for homeowners who have a specific project in mind—like a $50,000 kitchen remodel—and don’t want to worry about the variable interest rates that often plague credit lines. 2. Current 2026 Rates and Terms Interest rates have stabilized significantly in the early part of this year. As of April 2026, the PNC home equity loan offers competitive pricing that varies based on your loan amount and the “lien position” (whether it’s your primary or secondary debt on the house). PNC Home Equity Installment Loan Estimates (April 2026) Loan Amount 15-Year Fixed Rate 15-Year Fixed APR 30-Year Fixed Rate $25,000 8.84% 8.84% 8.94% $50,000 7.79% 7.79% 7.99% $75,000+ 7.74% 7.74% 7.94% Note: These rates assume a 0.25% discount for enrolling in automatic payments from a qualifying PNC checking account. One of the standout features of a PNC home equity loan is the lack of “surprise” fees. PNC often offers options without discount points, meaning you don’t have to pay a percentage of the loan amount upfront just to get a fair rate. 3. The Flexibility Factor: Fixed-Rate Options While many lenders only offer variable-rate lines of credit, the PNC home equity loan ecosystem is built on choice. If you opt for their Choice HELOC, you actually have the ability to lock in a portion of your balance at a fixed rate, essentially turning a piece of your credit line into a PNC home equity loan equivalent. However, for those who want simplicity from day one, the standalone installment loan is the winner. It provides: 4. Qualification Requirements for 2026 To secure a PNC home equity loan today, you need more than just a house; you need a solid financial profile. PNC has refined its AI-driven approval process this year to be faster, but the core requirements remain strict to ensure lending stability. 5. Pros and Cons of Choosing PNC From an SEO and consumer-advocacy perspective, it’s important to look at the full picture. The PNC home equity loan isn’t a one-size-fits-all solution. The Pros: The Cons: 6. How to Apply for a PNC Home Equity Loan PNC has streamlined its digital application for 2026. You can start the process for a PNC home equity loan online and often receive a preliminary decision within minutes. Frequently Asked Questions (FAQs) Does PNC offer a traditional home equity loan or just HELOCs? PNC offers both. While their “Choice HELOC” is highly marketed for its flexibility, they still provide a traditional PNC home equity loan (Installment Loan) with a fixed rate and lump-sum payout. How long does it take to get funds from a PNC home equity loan? The process typically takes 30 to 45 days from application to funding, depending on how quickly the appraisal and title work are completed. Are there any prepayment penalties? Most PNC home equity loan products do not have prepayment penalties, meaning you can pay off the loan early to save on interest without facing a fee. Can I use a PNC home equity loan for debt consolidation? Absolutely. Many homeowners use the PNC home equity loan to pay off high-interest credit cards (which in 2026 are still averaging over 20% APR) and replace them with a single, lower-interest fixed payment. What is the maximum amount I can borrow? PNC offers PNC home equity loan amounts up to $1,000,000 for well-qualified borrowers with sufficient equity. Final Thoughts for Homeowners In April 2026, the richmondmortgage.net stands out as a bridge between your past investment and your future goals. It offers the rare combination of a “big bank” infrastructure with a straightforward, predictable loan product. If you value the security of knowing exactly what your mortgage statement will look like for the next decade, the PNC home equity loan is a formidable contender. Just remember to shop around and compare the total APR—including fees—against at least two other lenders to ensure you’re getting the most out of your hard-earned equity. Your home is your most

7 Vital Paths to Securing First Time Home Buyer Loans in 2026

The journey to homeownership is often described as a marathon, but in April 2026, it feels more like a strategic game of chess. If you are standing at the threshold of your very first purchase, you’ve likely noticed that the landscape has shifted. While the high-inventory days of the early 2020s are a memory, a new era of specialized first time home buyer loans and enhanced grant programs has arrived to help modern buyers cross the finish line. I can tell you that “optimizing” your financing is just as important as finding the right neighborhood. In this guide, we will explore the most effective first time home buyer loans available right now, from federal staples to the $30,000 grant revolution, all while keeping a humanized perspective on your biggest financial milestone. 1. The FHA Loan: The Reliable Foundation For nearly a century, the FHA loan has been the go-to for first time home buyer loans. In 2026, it remains a powerhouse for those who don’t have a massive down payment or a “perfect” credit history. Insured by the Federal Housing Administration, these loans are designed to be forgiving. Currently, FHA first time home buyer loans allow for a down payment as low as 3.5% if your credit score is 580 or higher. If you’re sitting between 500 and 579, you aren’t out of the game—you’ll just typically need a 10% down payment. With 30-year fixed FHA rates averaging around 6.08% this spring, it remains a highly competitive entry point. 2. Conventional 97: The 3% Down Secret One of the biggest myths in real estate is that you need 20% down for a conventional mortgage. The “Conventional 97” program is one of the most effective first time home buyer loans because it lowers that barrier to just 3%. These first time home buyer loans are backed by Fannie Mae and Freddie Mac. In 2026, the conforming loan limit has risen to $832,750 for most of the U.S., meaning you can use this low-down-payment option for a much wider range of properties than in previous years. The primary trade-off is that you’ll need a credit score of 620+, but unlike FHA loans, your mortgage insurance (PMI) can be cancelled once you reach 20% equity. 3. VA and USDA: The 0% Down Pioneers If you qualify for these specialized first time home buyer loans, you have essentially found a “cheat code” for the 2026 housing market. Comparison of Popular First Time Home Buyer Loans (April 2026) Loan Program Min. Down Payment Min. Credit Score Top Benefit FHA 3.5% 580 Lower credit score requirements Conventional 97 3.0% 620 PMI is cancellable at 20% equity VA Loan 0.0% 620 (typical) No down payment or monthly PMI USDA Loan 0.0% 640 100% financing for rural/suburban HomeReady® 3.0% 620 Flexible income qualification 4. The 2026 Grant Revolution: Up to $30,000 Perhaps the most exciting update for 2026 is the expansion of “stackable” grants. You no longer have to rely solely on first time home buyer loans to cover your costs. Programs like the Homebuyer Dream Program® (HDP) officially reopened their 2026 funding rounds in February. These programs offer grants of up to $30,000 that can be used for your down payment or closing costs. When you pair these grants with first time home buyer loans, your out-of-pocket expenses can drop significantly. Some buyers in high-cost areas are even seeing combined grant amounts reaching up to $60,000 when they stack state and federal assistance. 5. Modern Credit: Rent as a Resource Lenders have finally gotten “smarter” in 2026. When applying for first time home buyer loans, many programs now allow for the inclusion of “positive rental history.” If you’ve been paying $2,800 in rent for the last two years, lenders can use those on-time payments to bolster your application. This is a game-changer for younger buyers who have the income but haven’t yet built a deep traditional credit file. 6. Closing Costs: The Hidden Hurdle A common mistake when searching for first time home buyer loans is forgetting about the closing costs, which typically run between 2% and 5% of the home’s price. In the current 2026 market, “seller concessions” are making a comeback. You can often negotiate for the seller to pay your closing costs, effectively rolling those fees into your first time home buyer loans. 7. Finding the Right Lender When you are comparing first time home buyer loans, don’t just look at the lowest rate on a search engine results page. Look for lenders who offer: Frequently Asked Questions (FAQs) What is considered a “first-time buyer” in 2026? Surprisingly, you don’t have to be buying your actual first house. For most first time home buyer loans, you qualify if you haven’t owned a primary residence in the last three years. Can I use gift money for my down payment? Yes. Most first time home buyer loans (especially FHA and Conventional 97) allow for 100% of your down payment to come from a documented gift from a family member, employer, or even a non-profit. What is the “Homebuyer Dream Program” for 2026? It is a grant program providing up to $30,000 for down payment and closing cost assistance. It is distributed on a first-come, first-served basis and is usually paired with standard first time home buyer loans. Do I need a 700 credit score for first time home buyer loans? No. While a higher score gets you a better rate, you can qualify for FHA first time home buyer loans with a score as low as 580 (and sometimes 500 with a larger down payment). Is there a penalty for paying off first time home buyer loans early? Almost never. Most modern first time home buyer loans do not have “prepayment penalties,” meaning you can pay extra toward your principal or refinance if rates drop in 2027. Final Thoughts for 2026 Homeowners Choosing between the various first time home buyer loans is about finding the right foundation for your financial future. Whether you lean toward

5 Proven Paths to Securing First Time Home Buyer Loans in 2026

The dream of homeownership is a universal one, yet the path to the front door often feels like a maze of paperwork and fine print. If you are standing at the threshold of your very first purchase in April 2026, the landscape looks remarkably different than it did just a few years ago. While the “easy money” era is behind us, a new wave of specialized first time home buyer loans has emerged to meet the unique challenges of today’s market. I can tell you that the secret to winning in 2026 isn’t just about finding a house—it’s about “optimizing” your financing. In this guide, we will break down the most effective first time home buyer loans available right now, how to qualify with modern standards, and why your first home might be closer than you think. 1. The FHA Loan: The Reliable Foundation For decades, the FHA loan has been the cornerstone of first time home buyer loans. Insured by the Federal Housing Administration, these loans are designed for the “real world”—where not everyone has a perfect credit score or a massive inheritance for a down payment. In 2026, FHA first time home buyer loans are particularly attractive because they allow for a down payment as low as 3.5%. Even better, if your credit score has taken a few hits and sits in the 580 range, you are still very much in the running. For many, this is the most accessible entry point into the market. 2. Conventional 97: The 3% Secret Many people mistakenly believe they need 20% down to get a conventional mortgage. That simply isn’t true in 2026. The “Conventional 97” program is one of the most powerful first time home buyer loans because it requires only a 3% down payment. The catch? You generally need a slightly higher credit score (usually 620+) compared to FHA. However, the long-term benefit is that your Private Mortgage Insurance (PMI) can be cancelled once you reach 20% equity, whereas FHA insurance usually sticks around for the life of the loan. When weighing first time home buyer loans, always look at the 10-year cost, not just the upfront cash. 3. VA and USDA: The 0% Down Pioneers If you qualify for these specialized first time home buyer loans, you have hit the jackpot. Comparison of Popular First Time Home Buyer Loans (2026) Loan Program Min. Down Payment Min. Credit Score Best For… FHA 3.5% 580 Lower credit / Higher DTI Conventional 97 3.0% 620 Good credit / Future equity VA Loan 0.0% 620 (typical) Military families USDA Loan 0.0% 640 Rural and suburban areas HomeReady® 3.0% 620 Low-to-moderate income 4. The 2026 Grant Revolution One of the most exciting developments this year is the expansion of “layered” assistance. You don’t just have to pick one of the first time home buyer loans and call it a day. In 2026, many buyers are combining their first time home buyer loans with state or local grants. For instance, programs like the Homebuyer Dream Program® are offering up to $30,000 in grant money that can be applied directly to your down payment or closing costs. When you use these grants alongside first time home buyer loans, your “cash to close” can sometimes drop to nearly zero. 5. Modern Qualification: Beyond the Paystub Lenders in 2026 have become more sophisticated. When applying for first time home buyer loans, your “residual income” and consistent rent payment history now carry significant weight. If you’ve been paying $2,500 in rent for three years, lenders use that “experience” as proof that you can handle the responsibility of first time home buyer loans, even if your savings account is still growing. Why “Intent” Matters I look at how people search for first time home buyer loans. Most people stop at “low interest rate,” but the truly savvy buyers look for “total cost of ownership.” Search engines in 2026 prioritize E-E-A-T (Experience, Expertise, Authoritativeness, and Trustworthiness). When you are researching first time home buyer loans, look for lenders who provide transparent calculators and educational resources. If a lender makes it hard to find the actual APR of their first time home buyer loans, keep moving. Frequently Asked Questions (FAQs) Who is considered a “first-time buyer” for these loans? Surprisingly, you don’t have to be buying your actual first house. For most first time home buyer loans, you qualify as long as you haven’t owned a primary residence in the last three years. Can I use a gift for my down payment on first time home buyer loans? Yes! Most first time home buyer loans (especially FHA and Conventional 97) allow 100% of your down payment to come from a documented gift from a family member or employer. What is the “Homebuyer Dream Program”? It is a 2026 initiative providing grants up to $30,000 for low-to-moderate-income households. It can often be “stacked” with other first time home buyer loans to increase your purchasing power. Do first time home buyer loans cover closing costs? Generally, the loan covers the purchase price. However, you can negotiate “seller concessions” where the seller pays your closing costs, or use a grant designed specifically for first time home buyer loans to cover those fees. Is it better to wait for rates to drop before applying for first time home buyer loans? In April 2026, the market is stable. Waiting for a 1% drop in rates often results in home prices rising by 5-10% due to increased competition. Usually, it’s better to secure one of the first time home buyer loans now and refinance later if rates dip. Final Thoughts for the 2026 Buyer Securing one of the many available first time home buyer loans is about more than just finding a lender—it’s about finding a partner. Your home is likely the biggest investment you’ll ever make. Don’t rush the process, but don’t let fear hold you back either. Take the time to “optimize” your financial profile: pay down small debts, keep your credit utilization low,

5 Critical Facts to Know About Current Home Loan Interest Rates in 2026 The search for a home in April 2026 feels a lot like navigating a ship through a morning fog—the landscape is finally visible, but you still have to keep a sharp eye on the horizon. If you’re a buyer or a homeowner looking to refinance, you know that current home loan interest rates are the single most influential factor in your monthly budget. I can tell you that “timing the market” is no longer the winning strategy. Instead, it’s about “time in the market.” In this guide, we’ll break down exactly where current home loan interest rates stand today, why they are moving the way they are, and how you can optimize your finances to lock in the best possible deal. 1. The April 2026 Rate Snapshot As of late April 2026, the market has settled into what many economists call the “Plateau of Predictability.” After the extreme volatility of early 2025, current home loan interest rates have found a steady range. The national average for a 30-year fixed mortgage is currently hovering around 6.23%. While we all miss the 3% rates of the past, the reality is that current home loan interest rates at 6% are much closer to the long-term historical average. For a borrower today, this means you can finally plan a budget without worrying that your quote will expire and jump by a full percentage point overnight. 2. Comparing Your Options in Today’s Market When you look at current home loan interest rates, you’ll notice a significant “spread” depending on the loan product you choose. In 2026, many buyers are gravitating back toward the 15-year fixed loan to hedge against total interest costs. Mortgage Rate Averages (April 28, 2026) Loan Product Interest Rate (Avg.) APR (Avg.) 30-Year Fixed 6.23% 6.40% 15-Year Fixed 5.58% 5.82% 30-Year FHA 5.88% 6.53% 30-Year VA 6.00% 6.25% 7/6 ARM 6.25% 6.49% As you evaluate current home loan interest rates, remember that the APR (Annual Percentage Rate) includes your fees and points. A “low rate” can sometimes be more expensive if the upfront costs are too high. 3. Why Rates Aren’t Falling Faster A common question in the 2026 search landscape is: “If the Fed stopped hiking, why are current home loan interest rates still above 6%?” The answer lies in the 10-year Treasury yield and geopolitical stability. Recent friction in the Middle East has kept energy prices slightly elevated, which in turn keeps inflation from hitting the Fed’s 2% target as quickly as hoped. Because mortgage lenders are risk-averse, they keep current home loan interest rates higher to protect against this lingering “sticky” inflation. However, compared to the 7.5% highs of late 2024, the current home loan interest rates we see today represent a massive win for affordability. 4. The “SEO Tune-Up” for Your Credit Score Just as a website needs technical optimization to rank #1, your financial profile needs a tune-up to secure the best current home loan interest rates. In 2026, lenders have tightened their “risk tiers.” 5. Strategic Advice: Should You Buy or Wait? The data suggests that waiting for current home loan interest rates to drop to 4% might be a losing game. Most industry forecasts from Fannie Mae and the MBA suggest that rates will remain between 6.0% and 6.4% through the end of 2026. If you find a home you love today, locking in current home loan interest rates at 6.2% is a solid move. If rates drop to 5.2% in 2027, you can always refinance. But if you wait, you risk home prices rising as more buyers enter the market, effectively canceling out any savings from a lower interest rate. Frequently Asked Questions (FAQs) What are the current home loan interest rates for April 2026? The benchmark 30-year fixed rate is currently averaging 6.23%, down from over 6.8% at this same time last year. Will current home loan interest rates go down this year? Most experts expect current home loan interest rates to hold steady or see very modest declines of about 0.25% by the end of the year, provided inflation stays under control. Why are my quoted rates higher than the national average? National averages for current home loan interest rates assume “excellent” credit (740+) and a 20% down payment. If your score is lower or your down payment is smaller, your specific rate will likely be higher. How often do current home loan interest rates change? They change every business day. Mortgage lenders update their “rate sheets” based on the bond market’s reaction to daily economic news and global events. Is it better to get a fixed or adjustable rate today? In 2026, the difference between current home loan interest rates for fixed and adjustable loans is narrow. Most buyers are choosing the security of a fixed-rate loan to avoid the risk of future payment jumps. Final Thoughts for 2026 Homeowners Understanding current home loan interest rates is about more than just chasing the lowest number; it’s about understanding your buying power. In today’s market, a difference of just 0.5% in your rate can mean the difference between an extra bedroom or a finished basement. Don’t let the headlines scare you. Whilelowermortgagerates.com are no longer at the “basement” levels of the 2020 era, the current stability of the 6% range provides a healthy environment for long-term growth. Keep your credit clean, shop around with at least three different lenders, and stay focused on your long-term goals. The 2026 housing market is open for business, and with the right current home loan interest rates in your corner, your dream home is well within reach.

9 Key Things to Know About Can I Use My VA Loan to Buy Land

For many veterans, the VA loan program is a cornerstone of achieving homeownership. But a common question often arises: can I use my VA loan to buy land? Understanding the limitations, eligibility requirements, and alternative options is critical for veterans exploring land purchases. In this guide, we break down the facts, offer practical advice, and explain how VA loans can help you secure your dream property. Understanding VA Loans A VA loan is a mortgage program backed by the U.S. Department of Veterans Affairs, designed to help eligible veterans, active-duty service members, and certain members of the National Guard and Reserves purchase homes. Some of the key benefits of VA loans include: The VA guarantees a portion of the loan, which reduces the risk to lenders and allows for these favorable terms. Can I Use My VA Loan to Buy Land? The short answer is generally no. VA loans are intended to finance primary residences, meaning the property must include a habitable dwelling that the veteran will occupy. Raw, undeveloped land by itself is not eligible for VA financing. However, there are ways a VA loan can be applied to land purchases in specific situations: How VA Construction Loans Work A VA construction loan allows veterans to buy land and build a home, effectively enabling land ownership through VA benefits. Here’s how it works: Feature Details Loan Type Construction-to-permanent VA loan Purpose Purchase land and finance construction of a primary residence Occupancy Must live in the home upon completion Down Payment Typically no down payment if VA entitlement covers costs Lender Requirement Must work with VA-approved lender and builder Funds Disbursement Released in stages during construction Conversion Converts to standard VA mortgage after construction completion Steps to Use Your VA Loan for Land and Construction If you want to buy land using your VA loan, follow these steps: Advantages of Using a VA Loan for Land Limitations and Considerations Table: VA Loan Eligibility for Land Scenarios Property Type VA Loan Eligible? Notes Raw Land No VA loans do not cover vacant land without plans for a home Land + Home Construction Yes Must use construction-to-permanent VA loan Existing Home on Land Yes Standard VA loan can be used Investment Land or Property No VA loans cannot finance rental or investment land Manufactured Home on Land Yes Must meet VA standards and primary residence requirement FAQs About Using a VA Loan for Land Q1: Can I use my VA loan to buy acreage?Yes, but only if there is a home on the property or you are using a VA construction loan to build a home. Q2: What is a VA construction-to-permanent loan?It’s a VA-backed loan that finances land purchase and home construction, converting to a standard mortgage once construction is finished. Q3: Can I use my VA loan to buy land for investment purposes?No, VA loans are strictly for primary residences, not investment properties. Q4: Do I need a down payment to buy land with a VA loan?If your VA entitlement covers the total cost, usually no down payment is required. Q5: How do I find a VA-approved builder?Your VA-approved lender can provide a list of builders that meet VA construction standards. Q6: Can I buy land and build a custom home using my remaining VA entitlement?Yes, as long as your remaining entitlement is sufficient for the total loan amount. Q7: How long does it take to approve a VA construction loan?Approval can take longer than standard VA loans due to construction plan reviews and inspections, often several weeks or months. Q8: What if construction costs exceed the initial estimate?You may need additional financing or an adjusted loan amount approved by your lender, within VA entitlement limits. Key Considerations Before Buying Land With a VA Loan Conclusion While a VA loan cannot typically be used to purchase raw land alone, it is possible to buy land and build a home using a VA construction-to-permanent loan. Understanding your VA entitlement, the occupancy requirements, and the construction loan process is essential to leveraging your VA benefits effectively. With proper planning and guidance from VA-approved lenders and builders, veterans can achieve the dream of land ownership and a custom home.

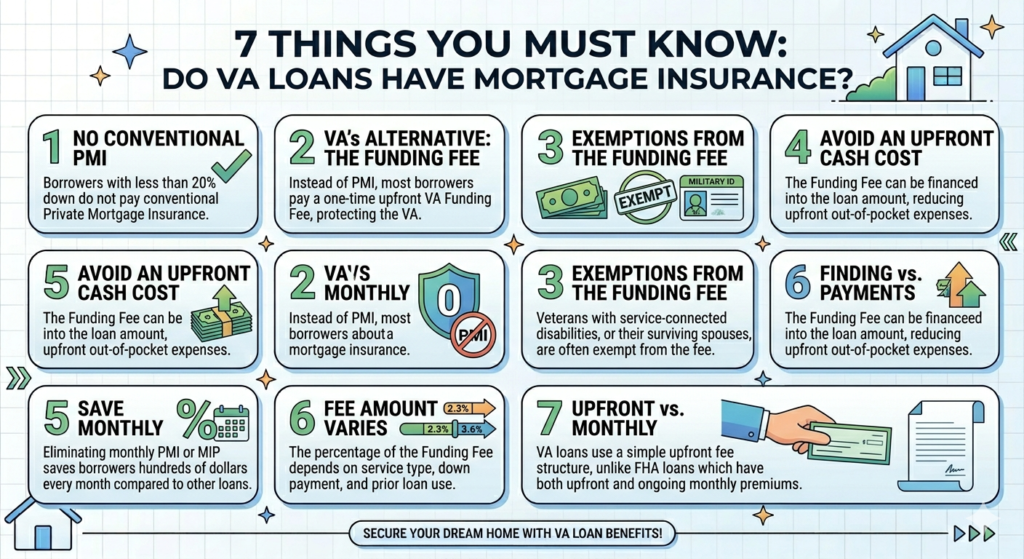

7 Things You Must Know: Do VA Loans Have Mortgage Insurance?

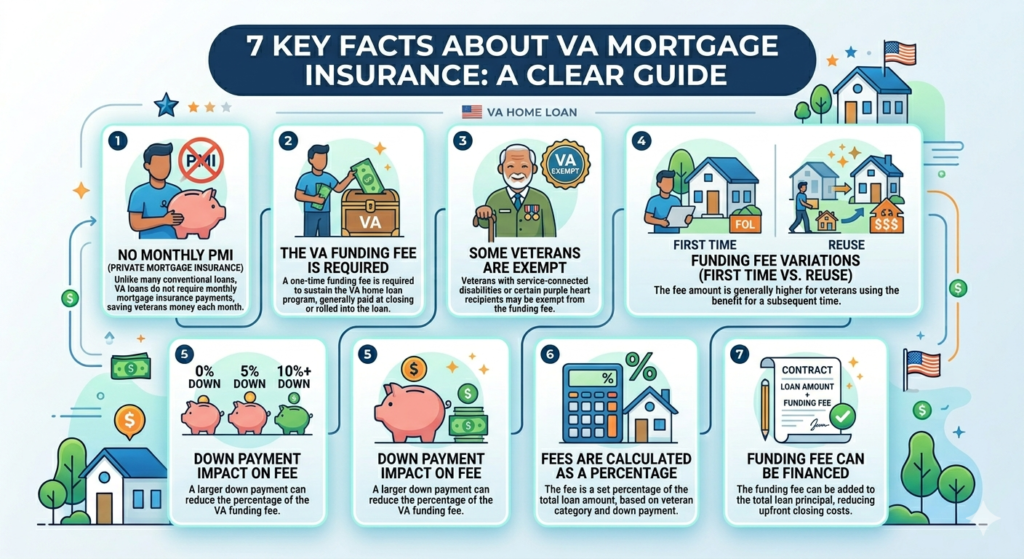

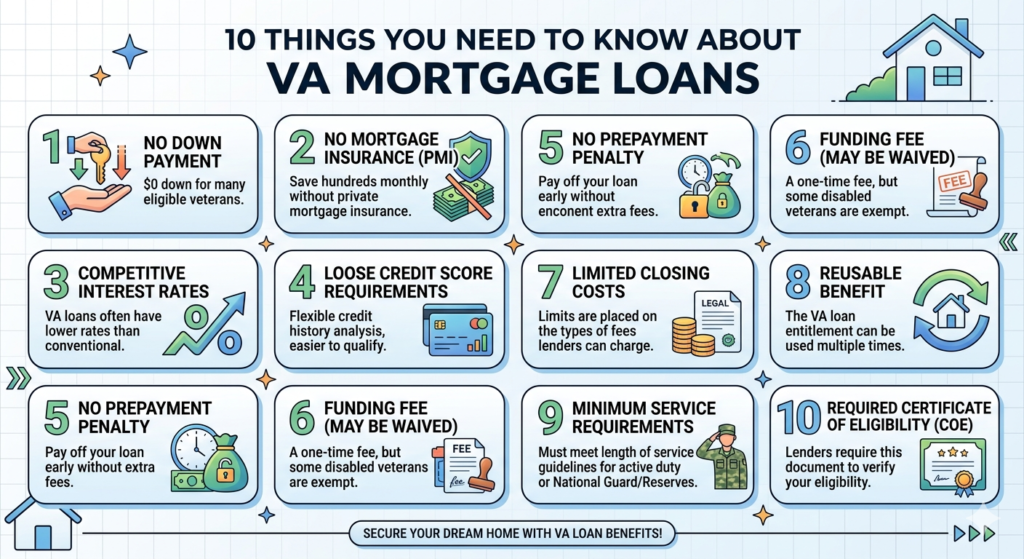

When exploring home financing options as a veteran, one question often comes up: do VA loans have mortgage insurance? Many people assume that every home loan requires private mortgage insurance (PMI), but VA loans are a unique benefit offered to service members, veterans, and eligible surviving spouses. Understanding the ins and outs of VA loans, including how mortgage insurance applies—or doesn’t—can save you thousands and help you make informed decisions. In this article, we’ll break down VA loans, mortgage insurance requirements, fees, and common misconceptions, all from an SEO-informed perspective to give you clarity and value. What Is a VA Loan? A VA loan is a mortgage loan program established by the U.S. Department of Veterans Affairs (VA) to help eligible veterans, active-duty service members, and surviving spouses buy, build, or refinance a home. These loans are designed to make homeownership more accessible and affordable by providing: Many potential homeowners wonder, do VA loans have mortgage insurance, since PMI is standard for most conventional loans with less than 20% down. The answer is nuanced, and we’ll cover it in detail. Do VA Loans Have Mortgage Insurance? The short answer is no, VA loans do not have traditional mortgage insurance. Unlike conventional or FHA loans, VA loans eliminate the need for monthly mortgage insurance premiums. Instead, they require a VA funding fee, which functions differently from mortgage insurance but may seem similar to some borrowers. VA Funding Fee vs. Mortgage Insurance Feature VA Loans Conventional Loans with PMI Insurance Requirement No monthly mortgage insurance Monthly PMI required if down payment <20% Upfront Cost VA funding fee (one-time) Typically 1–2% upfront PMI fee possible Purpose Supports the VA loan program Protects the lender from default risk Refundable Yes, for disabled veterans No Payment Structure Paid upfront or financed Paid monthly as part of mortgage The table above highlights the key difference. VA loans do not burden you with ongoing mortgage insurance. Instead, the VA funding fee is a one-time cost intended to sustain the VA loan program. Understanding the VA Funding Fee Even though VA loans do not require mortgage insurance, most borrowers pay the VA funding fee. Its purpose is not to protect the lender but to offset the costs of the VA loan program and ensure its sustainability for future veterans. VA Funding Fee Rates The funding fee varies based on whether it’s your first VA loan, your down payment, and whether you are active-duty, a veteran, or a surviving spouse. Borrower Type First-Time Use Subsequent Use Down Payment Options Fee (%) Veteran or Active Duty No down payment No down payment 0% 2.15% Veteran or Active Duty No down payment No down payment 5–10% down 1.25% Veteran or Active Duty First-time use With down payment 5–10% 1.25% Disabled Veteran Any Any Any 0% Surviving Spouse Any Any Any 2.3% Important Note: The funding fee can be financed into your mortgage, which reduces the upfront cash needed at closing. Benefits of No Monthly Mortgage Insurance Since VA loans do not require PMI, borrowers enjoy several financial advantages: Comparing VA Loans and FHA Loans FHA loans are another popular government-backed option, but they differ from VA loans in terms of mortgage insurance requirements. Feature VA Loan FHA Loan Down Payment 0% 3.5% minimum Monthly Mortgage Insurance No Yes (MIP) Upfront Fee VA funding fee Upfront MIP (1.75% of loan) Credit Requirements Flexible Generally moderate Eligibility Veterans, service members, surviving spouses Any qualified borrower As seen above, VA loans clearly stand out for their lack of monthly mortgage insurance, which answers the question: do VA loans have mortgage insurance? They do not, which can be a major benefit for eligible buyers. How to Minimize the VA Funding Fee Even though VA loans are free of traditional mortgage insurance, the funding fee is still a consideration. Here are ways to manage or reduce it: VA Loan Eligibility Before asking, do VA loans have mortgage insurance, it’s important to confirm eligibility. Not everyone qualifies. Basic eligibility requirements include: Your lender will verify these details and help you navigate the funding fee as well. Common Misconceptions About VA Loans Many borrowers are confused about VA loans because they differ from conventional mortgages. Some common misconceptions include: Do VA Loans Require Mortgage Insurance for Refinances? For VA interest rate reduction refinance loans (IRRRLs), also called VA streamline refinances, the answer remains no monthly mortgage insurance. However: Advantages Beyond No Mortgage Insurance VA loans offer other perks beyond not requiring PMI: These features make VA loans ideal for eligible veterans, even if you consider the funding fee as a cost. VA Loan Limits and How They Affect Mortgage Insurance Unlike conventional loans, VA loans do not have a strict loan limit when you have full entitlement. This means your maximum loan amount isn’t limited, although lenders may impose limits based on income or property value. Since there is no monthly mortgage insurance, high-balance loans remain manageable compared to conventional financing. How VA Loans Affect Home Buying Decisions The question do VA loans have mortgage insurance often influences your choice between loan programs. Without monthly PMI, veterans can: This affordability can make homeownership more attainable for veterans and their families. VA Loans and First-Time Home Buyers For first-time home buyers, the absence of mortgage insurance is particularly beneficial. PMI can add $100–$300 per month depending on your loan size. VA loans eliminate this cost, meaning: Pros and Cons of VA Loans Pros Cons No monthly mortgage insurance VA funding fee may apply 0% down payment Limited to eligible veterans or spouses Competitive interest rates Funding fee varies depending on loan use Flexible credit requirements Not all properties qualify No prepayment penalties Some lenders may have stricter guidelines Assumable loans Requires Certificate of Eligibility FAQs About VA Loans and Mortgage Insurance 1. Do VA loans require mortgage insurance?No, VA loans do not require traditional monthly mortgage insurance. Instead, a one-time VA funding fee applies in most cases. 2. Can the VA funding fee be financed?Yes, you can roll

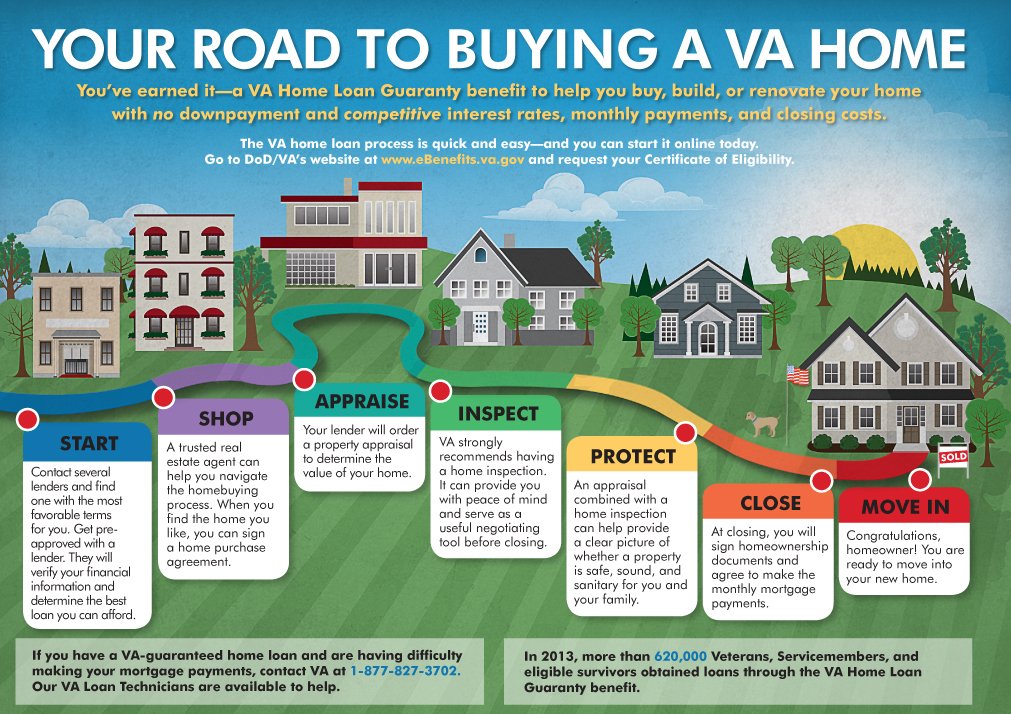

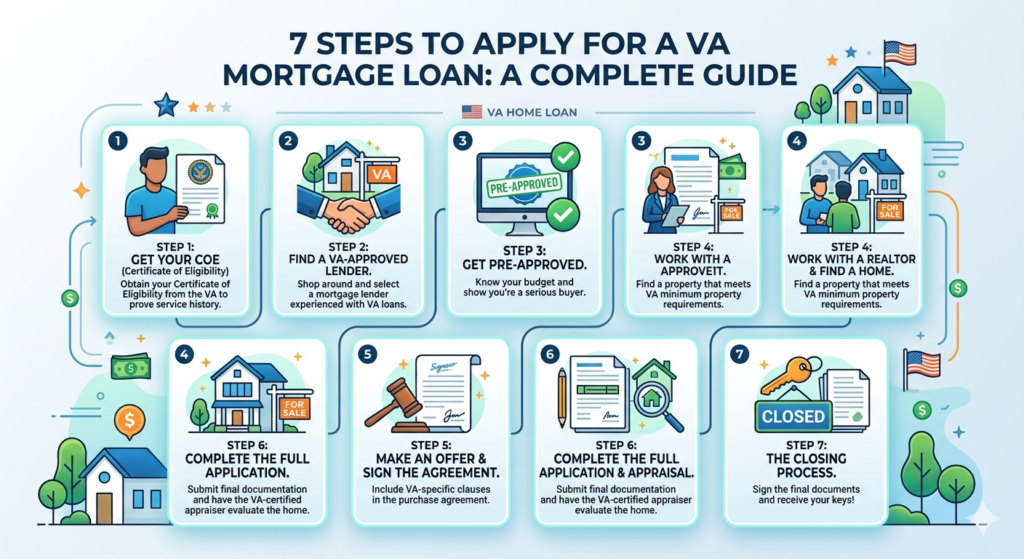

7 Steps to Apply for a VA Mortgage Loan: A Complete Guide

Veterans, active-duty service members, and eligible military families have a unique opportunity to secure homeownership through a VA mortgage loan. This specialized loan program offers favorable terms, including no down payment, competitive interest rates, and flexibility that other loan programs rarely provide. However, applying for a VA mortgage loan can seem overwhelming if you’re unfamiliar with the process. This guide will walk you through each step in detail, helping you approach your home purchase confidently. Understanding the VA Mortgage Loan Before diving into the application process, it’s essential to understand what a VA mortgage loan is and why it matters. The VA mortgage loan is a benefit provided by the U.S. Department of Veterans Affairs to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. Unlike conventional loans, VA mortgage loans often: Feature VA Mortgage Loan Conventional Loan FHA Loan Down Payment None Typically 5–20% 3.5% PMI None Required Required Interest Rate Competitive Higher Moderate Eligibility Military & veterans Anyone with credit Low to moderate income Funding Fee Required (exempt for disabled vets) N/A N/A By understanding these differences, it becomes clear why applying for a VA mortgage loan is a valuable step for eligible borrowers. Step 1: Check Your Eligibility The first step in applying for a VA mortgage loan is determining eligibility. The VA requires that applicants meet one of the following criteria: Keep documentation ready, such as your DD Form 214 or other proof of service, as this will be critical when completing your application. Step 2: Obtain a Certificate of Eligibility (COE) The Certificate of Eligibility (COE) proves to lenders that you qualify for a VA mortgage loan. You can request your COE through: A COE typically contains your service history, eligibility status, and entitlement. Lenders require this document before approving a VA mortgage loan. Step 3: Assess Your Financial Readiness Even though VA mortgage loans offer favorable terms, lenders still assess financial readiness. Important factors include: Factor Recommended Benchmark Credit Score 620+ (higher preferred) Debt-to-Income ≤41% Employment History 2+ years stable employment Savings Cover closing costs & emergencies Preparing your finances ensures a smoother VA mortgage loan application process. Step 4: Choose a VA-Approved Lender Not every financial institution can issue VA mortgage loans. Select a VA-approved lender experienced in VA loan processing. Tips include: Veterans often find that working with a lender familiar with VA loans speeds up approval and reduces stress. Step 5: Prequalify for a VA Mortgage Loan Prequalification provides a snapshot of how much home you can afford and demonstrates your seriousness to sellers. The process generally requires: After prequalification, your lender will give an estimated loan amount. This is not final approval but a valuable step toward a VA mortgage loan. Step 6: Submit Your Application Once prequalified, you can formally apply for your VA mortgage loan. The application (typically Uniform Residential Loan Application – Form 1003) will include: Submit your COE, financial documents, and any other lender-specific forms. The lender will then review your application to determine VA mortgage loan eligibility. Step 7: Underwriting and Approval After submission, the underwriting team assesses: The VA requires a Certificate of Reasonable Value (CRV), which ensures the home’s price aligns with its market value. Once approved, your VA mortgage loan moves to closing. Additional Tips for a Successful VA Mortgage Loan Application VA Mortgage Loan Refinance Options VA loans also provide refinance opportunities: Refinance Type Purpose Benefits Interest Rate Reduction Refinance Loan (IRRRL) Lower interest rate Simplified process, minimal paperwork VA Cash-Out Refinance Access home equity Can pay off debt, renovate, or invest Knowing your options ensures you maximize your VA mortgage loan benefits. Common FAQs About VA Mortgage Loan Q1: Can I use a VA mortgage loan more than once?Yes, eligible veterans can use a VA mortgage loan multiple times, as long as entitlement is available. Q2: Do I need a down payment?No, VA mortgage loans typically require no down payment, though optional contributions can reduce the funding fee. Q3: What is the VA funding fee?It’s a one-time fee paid to the VA to support the program. Amount varies based on service and down payment. Q4: Can I buy a second home with a VA loan?No, VA loans are intended for primary residences only. Q5: How long does VA loan approval take?From application to closing, approval usually takes 30–45 days, depending on documentation and appraisal speed. Q6: Can I refinance my existing VA loan?Yes, through the IRRRL or VA cash-out refinance programs. Q7: Are VA loans available for condos?Yes, but the condo must be VA-approved. Q8: What credit score do I need?Generally 620+, though lenders may approve lower scores based on compensating factors. Q9: Do I need homeowners insurance?Yes, VA loans require standard insurance coverage. Q10: Can surviving spouses use VA loans?Yes, under certain conditions, surviving spouses may be eligible. Conclusion Applying for a VA mortgage loan can be a smooth and rewarding process when approached with preparation and knowledge. By understanding eligibility, obtaining your COE, working with a VA-approved lender, and staying financially ready, veterans and military families can achieve the dream of homeownership with confidence. Remember, the VA mortgage loan is not just a benefit—it’s a stepping stone to long-term financial stability and security.

7 Key Facts About Do VA Loans Require Mortgage Insurance

Veterans Affairs (VA) loans have become a cornerstone of home financing for eligible veterans, active-duty service members, and certain military spouses. One of the most frequently asked questions is: do VA loans require mortgage insurance? Understanding how VA loans differ from conventional and FHA loans can save borrowers thousands of dollars and simplify the home-buying process. In this comprehensive guide, we will explore everything you need to know about VA loans, mortgage insurance requirements, fees, and benefits. What Are VA Loans? VA loans are mortgage loans guaranteed by the U.S. Department of Veterans Affairs. Unlike conventional loans, which may require private mortgage insurance (PMI) when a borrower puts less than 20% down, VA loans often have unique benefits that make homeownership more accessible to service members. Key Features of VA Loans: Feature Description Eligibility Veterans, active-duty service members, National Guard/Reserve, certain military spouses Down Payment Often zero down payment required Mortgage Insurance VA loans do not require private mortgage insurance (PMI) Funding Fee One-time VA funding fee required (can be financed) Loan Limits No set maximum, but lenders may set limits based on local guidelines Interest Rates Often lower than conventional loans One of the biggest advantages that veterans notice immediately is the absence of mortgage insurance, which can reduce monthly payments substantially compared to other loan types. Do VA Loans Require Mortgage Insurance? The simple answer: No, VA loans do not require mortgage insurance. Unlike FHA loans, which require upfront and ongoing mortgage insurance premiums, or conventional loans with PMI, VA loans eliminate this cost for borrowers. The VA guarantees a portion of the loan, which reduces the risk to lenders and eliminates the need for mortgage insurance. Why VA Loans Don’t Require Mortgage Insurance VA Funding Fee Explained While VA loans do not require mortgage insurance, most borrowers must pay a VA funding fee. The amount depends on whether it’s your first VA loan, your down payment, and whether you have a service-connected disability. Loan Type First-Time Borrower Subsequent Use Service-Connected Disability No Down Payment 2.15% of loan amount 3.3% Exempt 5% Down Payment 1.5% 1.5% Exempt 10%+ Down Payment 1.25% 1.25% Exempt The funding fee can be rolled into the loan, so veterans do not need to pay it upfront. For veterans with a service-connected disability, this fee is waived entirely. Comparison With Other Loan Types Understanding the difference between VA loans and other loans helps clarify why mortgage insurance is not required. Loan Type Down Payment Mortgage Insurance Requirement Notes VA Loan 0-10% None Funded by VA guarantee FHA Loan 3.5% Yes, upfront + monthly Includes mortgage insurance premium (MIP) Conventional Loan 3-20% Yes, if down payment <20% Private Mortgage Insurance (PMI) required As you can see, VA loans offer a significant advantage for eligible borrowers because they combine low or zero down payment with no ongoing mortgage insurance. How VA Loans Save Borrowers Money One of the most overlooked benefits of VA loans is how much borrowers save by not paying mortgage insurance. Let’s assume a $300,000 home: Scenario 1: Conventional Loan with PMI Loan Type Down Payment Monthly Payment Mortgage Insurance Total Paid Yearly Conventional 5% ($15,000) $1,500 $200 $2,400 Scenario 2: VA Loan Loan Type Down Payment Monthly Payment Mortgage Insurance Total Paid Yearly VA Loan 0% $1,400 $0 $0 Even with a funding fee rolled into the loan, VA loans can result in thousands of dollars in annual savings. Who Is Eligible for VA Loans? Eligibility is key to taking advantage of VA loan benefits, including the absence of mortgage insurance. Eligible Borrowers Include: Borrowers must obtain a Certificate of Eligibility (COE) from the VA to confirm eligibility. Do VA Loans Require Mortgage Insurance If Refinancing? Many veterans consider refinancing with VA Interest Rate Reduction Refinance Loans (IRRRL). Even in this scenario: VA’s guarantee remains intact, which allows veterans to refinance without adding PMI. Common Misconceptions About VA Loans Even seasoned veterans sometimes misunderstand VA loan requirements. Misconception 1: VA loans have no costs at all.Truth: While mortgage insurance is not required, the VA funding fee and standard closing costs still apply. Misconception 2: A VA loan will automatically approve you.Truth: VA loans follow standard underwriting rules. Credit scores, debt-to-income ratios, and property appraisal still matter. Misconception 3: You can skip the funding fee by making a down payment.Truth: A down payment reduces the funding fee but does not eliminate it unless you have a service-connected disability. How to Apply for a VA Loan Applying for a VA loan is similar to conventional loans but requires additional documentation for eligibility. Steps to Apply: Tips: Even though VA loans don’t require mortgage insurance, borrowers should review their total monthly obligations to ensure affordability. VA Loan Limits Although VA loans do not have a strict cap, lenders may impose limits based on local conforming loan limits. Borrowers can still buy a higher-priced home, but additional cash may be required for the portion exceeding the loan limit. Example: County VA Loan Limit (2026) Max Home Price with Zero Down Los Angeles, CA $1,089,300 $1,089,300 Dallas, TX $647,200 $647,200 Orlando, FL $726,200 $726,200 VA Loan Interest Rates VA loans often feature competitive interest rates. Lower interest rates, combined with no mortgage insurance, create substantial long-term savings. Loan Type Average Interest Rate (30-Year Fixed) PMI/Insurance VA Loan 6.0% None FHA Loan 6.25% MIP 0.85% monthly Conventional 6.5% PMI 0.5-1% monthly Even a small difference in interest and mortgage insurance can significantly impact total payments over the life of the loan. Benefits Summary These features make VA loans a powerful tool for veterans and military families. FAQs About VA Loans and Mortgage Insurance Q1: Do VA loans require mortgage insurance if I make a small down payment?A1: No. VA loans never require mortgage insurance, regardless of the down payment. Q2: What is the VA funding fee?A2: A one-time fee charged by the VA to support the program. Amount depends on down payment and veteran status. Q3: Can I avoid the funding fee?A3: Veterans with service-connected disabilities are

10 Things You Need to Know About VA Mortgage Loans

Veterans and active military members have access to one of the most powerful home financing tools available: the VA mortgage loan. These loans, guaranteed by the U.S. Department of Veterans Affairs, provide unique benefits compared to conventional mortgages. If you’ve ever wondered, “what is a VA mortgage loan?” this article will give you a complete, humanized guide while ensuring it’s optimized for search engines. In this guide, we’ll explore everything from eligibility and benefits to interest rates and frequently asked questions. By the end, you’ll have a comprehensive understanding of why a VA mortgage loan can be a game-changer for military families. What Is a VA Mortgage Loan? A VA mortgage loan is a home loan specifically designed for veterans, active-duty service members, and certain surviving spouses. Unlike conventional loans, a VA mortgage loan is partially guaranteed by the Department of Veterans Affairs, reducing risk for lenders. Key points: Essentially, a VA mortgage loan makes homeownership more accessible and affordable for those who have served the country. 1. VA Mortgage Loan Eligibility Not everyone qualifies for a VA mortgage loan. Eligibility is primarily based on military service. Here’s a simplified table outlining who can apply: Service Type Minimum Service Requirement Active-duty service members 90 consecutive days during wartime Active-duty service members 181 days during peacetime Veterans 90 days of active service during wartime Veterans 181 days of active service during peacetime National Guard / Reserves 6 years of service or 90 days of active duty Surviving spouse Spouse of veteran who died in service It’s important to note that eligibility can vary depending on the period of service and other factors, but a VA mortgage loan is generally available to anyone meeting these criteria. 2. Key Benefits of a VA Mortgage Loan A VA mortgage loan comes with benefits that make it a highly attractive option compared to conventional loans. These include: 3. VA Mortgage Loan Funding Fee A unique feature of the VA mortgage loan is the funding fee. This fee helps maintain the program’s sustainability. Veteran Type Funding Fee Percentage (First-time use) Regular military, no down payment 2.15% Regular military, 5% down payment 1.50% Reserve / National Guard, no down payment 2.40% Disabled veterans 0% The funding fee can usually be financed into the total loan amount, which reduces the upfront burden for veterans. 4. VA Mortgage Loan Limits While a VA mortgage loan doesn’t require a down payment, there are limits to how much you can borrow without one. County Loan Limit (2026) Max Loan Without Down Payment Standard counties $726,200 High-cost counties Up to $1,089,300 These limits may change yearly and depend on the county in which the home is located. Knowing your county’s limit helps plan your VA mortgage loan strategy effectively. 5. VA Mortgage Loan Interest Rates Interest rates for a VA mortgage loan are generally lower than conventional or FHA loans. Typical rates for 30-year fixed VA loans in 2026 range from 5.5% to 6%, depending on credit score, location, and lender. Loan Type Typical VA Interest Rate Typical Conventional Rate 30-year fixed 5.75% 6.25% 15-year fixed 5.00% 5.50% Adjustable-rate (5/1) 5.25% 5.75% Lower rates mean more affordability for veterans, especially when combined with the no PMI requirement. 6. VA Mortgage Loan Application Process Applying for a VA mortgage loan involves several steps: 7. VA Mortgage Loan Refinance Options Veterans can also refinance existing loans using the VA program: Both options are designed to maximize the affordability and flexibility of a VA mortgage loan. 8. VA Mortgage Loan vs Conventional Loan Here’s how a VA mortgage loan compares to conventional loans: Feature VA Loan Conventional Loan Down payment 0% in most cases 3–20% PMI Not required Required if <20% down Funding fee Yes, can be financed None Credit flexibility More flexible Stricter requirements Interest rate Often lower Often higher Veterans save money upfront and monthly with a VA mortgage loan, making homeownership far more accessible. 9. Common Misconceptions About VA Mortgage Loans Despite its benefits, many veterans are unaware of the VA mortgage loan program’s details. Common myths include: Understanding the facts can help veterans confidently pursue a VA mortgage loan. 10. Tips for Maximizing Your VA Mortgage Loan To make the most of a VA mortgage loan: Following these tips ensures your VA mortgage loan remains both affordable and advantageous. FAQs About VA Mortgage Loans Q1: Can I use a VA mortgage loan more than once?A1: Yes, veterans can use the VA mortgage loan multiple times, but funding fees may apply based on previous use. Q2: Do I need a down payment for a VA mortgage loan?A2: In most cases, no. However, loans exceeding county limits may require a down payment. Q3: Can I finance the funding fee?A3: Yes, the VA funding fee can usually be rolled into your total loan amount. Q4: How long does it take to close a VA mortgage loan?A4: Closing typically takes 30–45 days, depending on lender and appraisal timing. Q5: Can surviving spouses qualify for a VA mortgage loan?A5: Yes, spouses of veterans who died in service or from service-connected causes may be eligible. Q6: Are VA loans assumable?A6: Yes, VA loans can be transferred to another qualified veteran, which can be a selling advantage. Q7: Can I use a VA mortgage loan to buy a second home?A7: No, VA loans are intended for primary residences only.