Veterans Affairs (VA) loans have become a cornerstone of home financing for eligible veterans, active-duty service members, and certain military spouses. One of the most frequently asked questions is: do VA loans require mortgage insurance? Understanding how VA loans differ from conventional and FHA loans can save borrowers thousands of dollars and simplify the home-buying process. In this comprehensive guide, we will explore everything you need to know about VA loans, mortgage insurance requirements, fees, and benefits.

What Are VA Loans?

VA loans are mortgage loans guaranteed by the U.S. Department of Veterans Affairs. Unlike conventional loans, which may require private mortgage insurance (PMI) when a borrower puts less than 20% down, VA loans often have unique benefits that make homeownership more accessible to service members.

Key Features of VA Loans:

| Feature | Description |

|---|---|

| Eligibility | Veterans, active-duty service members, National Guard/Reserve, certain military spouses |

| Down Payment | Often zero down payment required |

| Mortgage Insurance | VA loans do not require private mortgage insurance (PMI) |

| Funding Fee | One-time VA funding fee required (can be financed) |

| Loan Limits | No set maximum, but lenders may set limits based on local guidelines |

| Interest Rates | Often lower than conventional loans |

One of the biggest advantages that veterans notice immediately is the absence of mortgage insurance, which can reduce monthly payments substantially compared to other loan types.

Do VA Loans Require Mortgage Insurance?

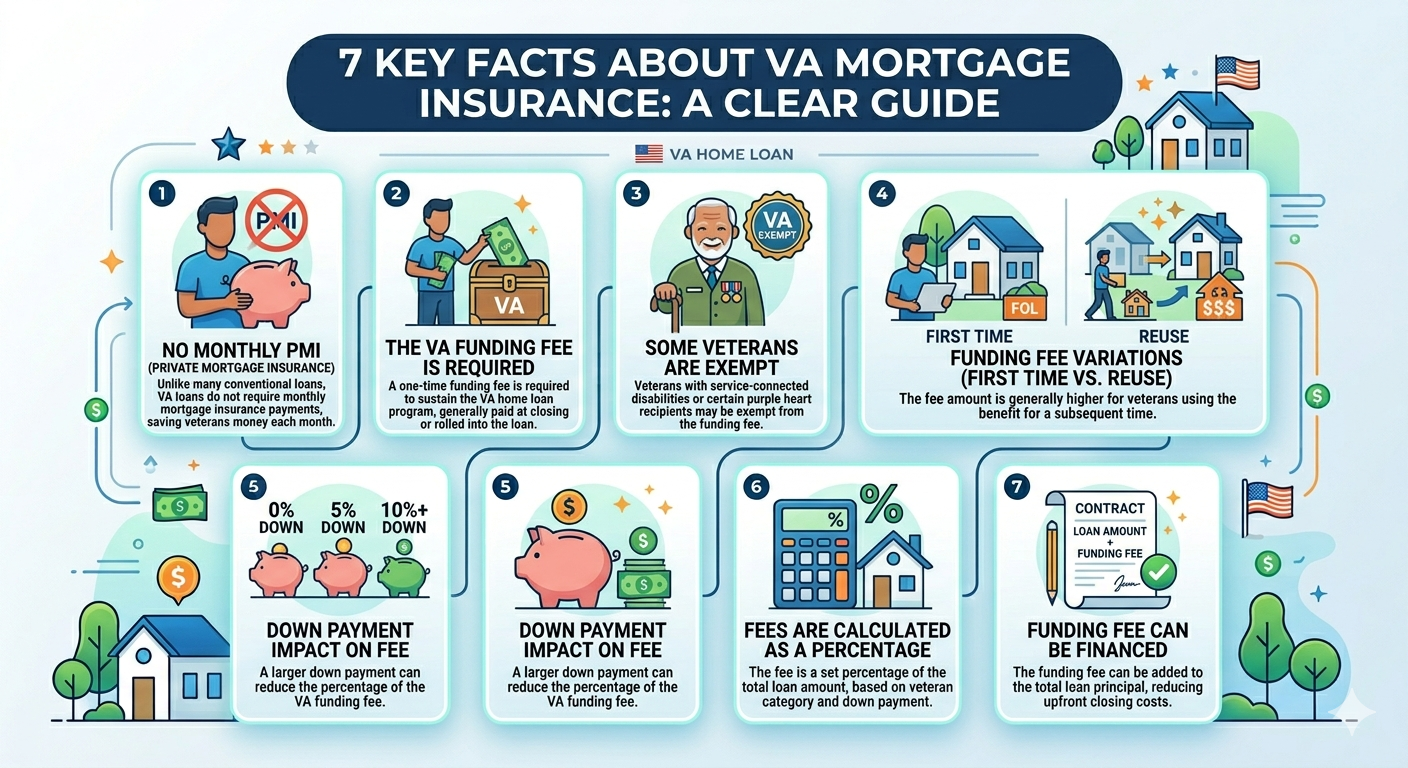

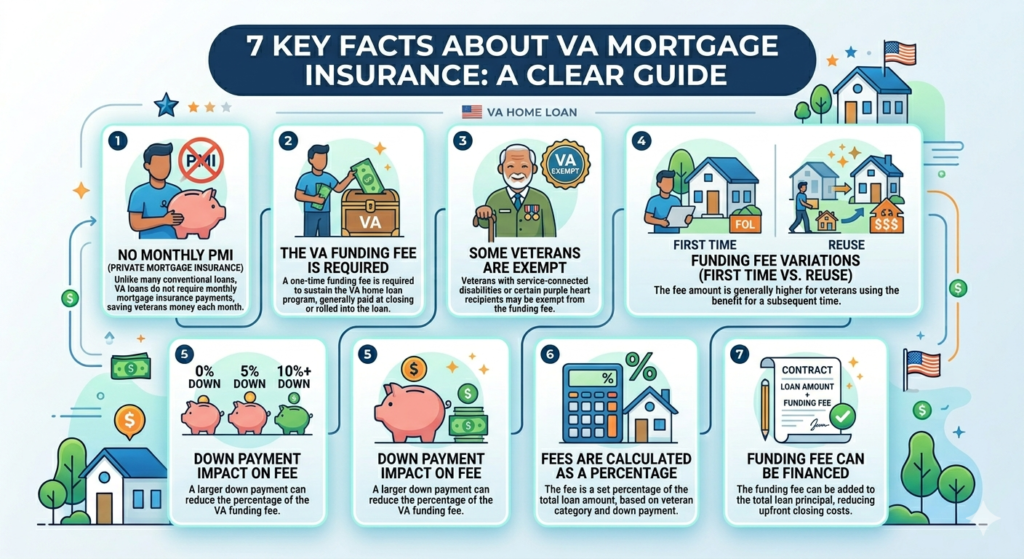

The simple answer: No, VA loans do not require mortgage insurance.

Unlike FHA loans, which require upfront and ongoing mortgage insurance premiums, or conventional loans with PMI, VA loans eliminate this cost for borrowers. The VA guarantees a portion of the loan, which reduces the risk to lenders and eliminates the need for mortgage insurance.

Why VA Loans Don’t Require Mortgage Insurance

- VA Guarantee: The VA guarantees a portion of the loan (usually 25%), which reassures lenders against loss.

- Funding Fee: Instead of monthly mortgage insurance, the VA charges a one-time funding fee. This fee supports the VA loan program and helps keep it sustainable.

VA Funding Fee Explained

While VA loans do not require mortgage insurance, most borrowers must pay a VA funding fee. The amount depends on whether it’s your first VA loan, your down payment, and whether you have a service-connected disability.

| Loan Type | First-Time Borrower | Subsequent Use | Service-Connected Disability |

|---|---|---|---|

| No Down Payment | 2.15% of loan amount | 3.3% | Exempt |

| 5% Down Payment | 1.5% | 1.5% | Exempt |

| 10%+ Down Payment | 1.25% | 1.25% | Exempt |

The funding fee can be rolled into the loan, so veterans do not need to pay it upfront. For veterans with a service-connected disability, this fee is waived entirely.

Comparison With Other Loan Types

Understanding the difference between VA loans and other loans helps clarify why mortgage insurance is not required.

| Loan Type | Down Payment | Mortgage Insurance Requirement | Notes |

|---|---|---|---|

| VA Loan | 0-10% | None | Funded by VA guarantee |

| FHA Loan | 3.5% | Yes, upfront + monthly | Includes mortgage insurance premium (MIP) |

| Conventional Loan | 3-20% | Yes, if down payment <20% | Private Mortgage Insurance (PMI) required |

As you can see, VA loans offer a significant advantage for eligible borrowers because they combine low or zero down payment with no ongoing mortgage insurance.

How VA Loans Save Borrowers Money

One of the most overlooked benefits of VA loans is how much borrowers save by not paying mortgage insurance. Let’s assume a $300,000 home:

Scenario 1: Conventional Loan with PMI

| Loan Type | Down Payment | Monthly Payment | Mortgage Insurance | Total Paid Yearly |

|---|---|---|---|---|

| Conventional | 5% ($15,000) | $1,500 | $200 | $2,400 |

Scenario 2: VA Loan

| Loan Type | Down Payment | Monthly Payment | Mortgage Insurance | Total Paid Yearly |

|---|---|---|---|---|

| VA Loan | 0% | $1,400 | $0 | $0 |

Even with a funding fee rolled into the loan, VA loans can result in thousands of dollars in annual savings.

Who Is Eligible for VA Loans?

Eligibility is key to taking advantage of VA loan benefits, including the absence of mortgage insurance.

Eligible Borrowers Include:

- Veterans with at least 90 consecutive days of active service during wartime or 181 days during peacetime.

- Current active-duty service members.

- National Guard and Reserve members meeting minimum service requirements.

- Certain surviving spouses of veterans who died in service or due to service-connected disabilities.

Borrowers must obtain a Certificate of Eligibility (COE) from the VA to confirm eligibility.

Do VA Loans Require Mortgage Insurance If Refinancing?

Many veterans consider refinancing with VA Interest Rate Reduction Refinance Loans (IRRRL). Even in this scenario:

- VA loans continue to not require mortgage insurance.

- The borrower may pay a minimal VA funding fee for the refinance, but this is generally lower than mortgage insurance premiums.

VA’s guarantee remains intact, which allows veterans to refinance without adding PMI.

Common Misconceptions About VA Loans

Even seasoned veterans sometimes misunderstand VA loan requirements.

Misconception 1: VA loans have no costs at all.

Truth: While mortgage insurance is not required, the VA funding fee and standard closing costs still apply.

Misconception 2: A VA loan will automatically approve you.

Truth: VA loans follow standard underwriting rules. Credit scores, debt-to-income ratios, and property appraisal still matter.

Misconception 3: You can skip the funding fee by making a down payment.

Truth: A down payment reduces the funding fee but does not eliminate it unless you have a service-connected disability.

How to Apply for a VA Loan

Applying for a VA loan is similar to conventional loans but requires additional documentation for eligibility.

Steps to Apply:

- Obtain a Certificate of Eligibility (COE) from the VA.

- Find a VA-approved lender.

- Submit a loan application with income, credit, and property details.

- Complete the VA appraisal and inspection process.

- Close on your home.

Tips: Even though VA loans don’t require mortgage insurance, borrowers should review their total monthly obligations to ensure affordability.

VA Loan Limits

Although VA loans do not have a strict cap, lenders may impose limits based on local conforming loan limits. Borrowers can still buy a higher-priced home, but additional cash may be required for the portion exceeding the loan limit.

Example:

| County | VA Loan Limit (2026) | Max Home Price with Zero Down |

|---|---|---|

| Los Angeles, CA | $1,089,300 | $1,089,300 |

| Dallas, TX | $647,200 | $647,200 |

| Orlando, FL | $726,200 | $726,200 |

VA Loan Interest Rates

VA loans often feature competitive interest rates. Lower interest rates, combined with no mortgage insurance, create substantial long-term savings.

| Loan Type | Average Interest Rate (30-Year Fixed) | PMI/Insurance |

|---|---|---|

| VA Loan | 6.0% | None |

| FHA Loan | 6.25% | MIP 0.85% monthly |

| Conventional | 6.5% | PMI 0.5-1% monthly |

Even a small difference in interest and mortgage insurance can significantly impact total payments over the life of the loan.

Benefits Summary

- No private mortgage insurance (PMI).

- Low or zero down payment.

- VA funding fee can be financed.

- Competitive interest rates.

- Flexible credit requirements.

These features make VA loans a powerful tool for veterans and military families.

FAQs About VA Loans and Mortgage Insurance

Q1: Do VA loans require mortgage insurance if I make a small down payment?

A1: No. VA loans never require mortgage insurance, regardless of the down payment.

Q2: What is the VA funding fee?

A2: A one-time fee charged by the VA to support the program. Amount depends on down payment and veteran status.

Q3: Can I avoid the funding fee?

A3: Veterans with service-connected disabilities are exempt.

Q4: Do I need mortgage insurance when refinancing a VA loan?

A4: No. VA refinancing loans do not require mortgage insurance.

Q5: How much can I borrow with a VA loan?

A5: VA loans do not have a strict cap, but lenders may set limits based on local guidelines.

Q6: Is VA loan approval guaranteed?

A6: No. Borrowers must meet credit, income, and property requirements.

Q7: Can I combine VA loans with other programs?

A7: Yes, but eligibility and benefits vary. It’s best to consult a VA-approved lender.

Conclusion

If you’ve been wondering, do VA loans require mortgage insurance, the answer is a resounding no. VA loans provide veterans, active-duty service members, and eligible spouses with a unique opportunity to buy a home with low upfront costs and substantial savings. By eliminating the need for private mortgage insurance and offering competitive interest rates, VA loans make homeownership more affordable and achievable. Veterans should always review their funding fee options and consult with a VA-approved lender to maximize the program’s benefits.