8 Reasons Glen Allen Homebuyers Choose GlenAllenMortgage.com Over the Big Names

Glen Allen homebuyers comparing mortgage lenders will find an honest, data-driven breakdown of why GlenAllenMortgage.com—led by award-winning broker Duane Buziak (NMLS#1110647)—consistently outperforms national giants like Rocket Mortgage and regional competitors across rate competitiveness, loan program flexibility, and personalized service in the Henrico County market.

Soft Pull Mortgage Prequalification: How Glen Allen Homebuyers Can Shop Rates Without Touching Their Credit Score

Glen Allen homebuyers can explore mortgage options and compare lender rates without damaging their credit score using soft pull mortgage prequalification, a largely misunderstood tool that separates initial rate shopping from formal application. This guide explains exactly how soft pulls differ from hard inquiries, what they reveal about your loan eligibility, and how Henrico County borrowers near Short Pump and Innsbrook can use this approach to confidently secure better terms.

Cash Out Refinance 90 Percent: How Glen Allen Homeowners Access More Equity Than Most Lenders Allow

Glen Allen homeowners with strong equity often hit an artificial 80% LTV ceiling imposed by banks—not by law—leaving tens of thousands of dollars inaccessible. This guide explains how a cash out refinance 90 percent LTV product works, who qualifies based on credit score, loan type, and property value, and how Henrico County borrowers can unlock significantly more equity than most national lenders will offer.

7 Proven Strategies Glen Allen Homebuyers Use to Win With a Top-Ranked Mortgage Broker

Duane Buziak of Glen Allen Mortgage earned back-to-back Scotsman Guide Top Originator recognition and triple UWM Awards, backed by $51.2 million in verified loan volume — and this guide breaks down the seven proven strategies Glen Allen homebuyers use to leverage a nationally ranked Glen Allen, Virginia based Mortgage Broker Of The Year to secure better rates, stronger pre-approvals, and a competitive edge in Henrico County’s active housing market.

Renovation Loan Fixer Upper: How to Finance a Home That Needs Work in Virginia

Renovation loan fixer upper financing solves the common problem Virginia buyers face when a property won’t qualify for a standard mortgage due to its condition—by wrapping the purchase price and repair costs into a single loan with one closing and one monthly payment. Programs like FHA 203(k) and Fannie Mae HomeStyle let buyers in markets like Glen Allen and Short Pump turn underpriced, needs-work properties into equity-building opportunities without requiring separate renovation savings.

7 Proven Strategies to Find the Best Mortgage Rates in Richmond, VA

In Richmond, VA’s competitive housing market, securing the best mortgage rates requires strategic shopping across multiple lenders — a quarter-point difference can save tens of thousands over a 30-year loan. This guide outlines seven proven strategies Richmond homebuyers use to compare offers, leverage broker access, and negotiate better terms without overpaying.

Duane Buziak Mortgage Maestro: 2026 Richmond’s Best Mortgage Rate Leader

Executive Summar Richmond, Virginia’s housing market is in flux in 2026. Inventory is climbing, and for the first time in years, mortgage rates have dipped under 6%. In this environment, local mortgage experts have become vital for buyers who want to save money and act quickly. Duane Buziak—known as the “Mortgage Maestro” with Coast2Coast Mortgage—has become one of the most trusted brokers in the Richmond area. This piece takes an in-depth look at how Buziak works, including his popular “NoTouch” estimate, wide array of loan options, and his client-first approach that’s earned national praise. Whether you’re buying your first home, self-employed and tired of rejection, or looking to invest in property in Virginia, Tennessee, Georgia, or Florida, you’ll find practical advice here for getting through this year’s mortgage hurdles. Duane Buziak Mortgage Maestro: 2026 Richmond’s Best Mortgage Rate Leader Introduction Imagine a longtime Richmond homebuyer who spots her dream house but isn’t sure if now is the best time to lock in a mortgage rate. At the same time, a self-employed business owner, frustrated with banks that reject her for having nontraditional income, starts to doubt whether she’ll ever own a home. Scenarios like these aren’t rare. The Richmond mortgage world is changing fast. The old “big bank” model no longer fits everyone. Today, local mortgage brokers like Duane Buziak are offering more than just lower rates—they provide a variety of loan choices and honest advice, tailored for each buyer. With more homes on the market, but prices still high, having a sharp broker isn’t just about getting a good rate—they can open new doors and make the process smoother. This guide explains why Buziak’s way of working is especially valuable now. You’ll get a clear sense of Richmond’s market, see how the “Mortgage Maestro” stands out, and find hands-on tips for your mortgage shopping journey. Market Insights Richmond’s 2026 housing market is full of contrasts. Suburbs like Glen Allen, Short Pump, and Midlothian have seen listings jump by 140% since 2022. Yet, prices haven’t dropped as much as expected because many homeowners simply won’t move unless they get their price, having locked in low rates years ago. Rate Environment: Mortgage rates have fallen below 6%, something we haven’t seen in over three years. Buyers now benefit from having more homes to pick from and lower borrowing costs, whether they’re looking to refinance or buy something new. This drop has especially motivated people wanting to “move up” to bigger homes and those looking to lower their high 2023–2024 loan payments. The Broker Advantage: While banks tend to move slowly and offer just a handful of loan options, independent brokers like Buziak play a different role. They connect with dozens of wholesale lenders, know the ins and outs of different loan programs, and can often get things done faster and with more flexibility than the traditional banks. Who Benefits: The wider pool of loan options makes a big difference for: In this market, the best rate is just part of the puzzle. The right loan fit, a speedy process, and expert advice are just as important as the percentage you see advertised. Product Relevance Duane Buziak’s “Mortgage Maestro” approach is simple: use smart technology, open up the full range of loan options, and offer real, honest guidance—especially for those overlooked by traditional lenders. The “NoTouch” Estimate System A standout feature is the “NoTouch” estimate. This service lets you get a quick look at your credit and estimated monthly payments—without a hard hit to your FICO. Here’s why it works: For example, a first-time buyer looking at condos in Richmond could use the NoTouch system to easily compare FHA, VA, and Conventional loan options at a 5.95% rate—without committing to a full application. Rate Shopping & Optimization Brokers like Buziak are especially good at finding the right rates. Instead of pushing a single product, he pulls quotes from several wholesale lenders to match each borrower’s unique profile. That flexibility matters in 2026, when even a quarter-point difference can save thousands of dollars down the line. This approach is a game-changer for: Specialized Loan Portfolio Duane Buziak is also known for his Non-QM (Non-Qualified Mortgage) offerings, designed for borrowers outside the usual mold: Anecdote: Case in point: a Richmond bakery owner, who’d been denied by several lenders over her reported income, was walked through the bank statement loan process and closed in 16 days—she finally bought her place after years of renting. Service Model: E-E-A-T in Action Here’s what stands out about Buziak’s record: Actionable Tips You need more than a low interest rate in 2026’s mortgage market. Here are practical steps for Virginia buyers thinking of using a broker like Buziak: 1. Use Pre-Qualification Strategically Start with tools like the NoTouch estimate if you want to see your options with zero credit impact. This is ideal for early planning, but you’ll need full pre-approval before making real offers in fast-moving areas like Short Pump or Midlothian. 2. Compare Programs, Not Just Rates Look beyond the interest rate: 3. Understand Trade-Offs No loan option is perfect. Independent brokers can get you more choices, but sometimes their total fees or closing costs are a bit higher. Rarely, a straightforward borrower may snag a slightly better deal at a local credit union. Always review the Loan Estimate, check the total costs, and watch out for rates that seem too good to be true. 4. Don’t Wait for the Absolute Bottom According to Realtor.com, price corrections typically lag behind market trends. If you keep waiting for rates to bottom out, you might lose your shot at the home you really want. If you find a home that fits your needs and budget, consider buying now and refinancing if rates drop later. 5. Evaluate Service as Much as Pricing The real strength of a good broker is their guidance and ability to solve unexpected problems quickly. Check reviews, ask about how they communicate (Buziak is known for being energetic and quick to respond—some love this pace,

10 Easy Ways to Lower First-Year Mortgage Costs

Buying a house is an exciting milestone, but the first year of homeownership can also be financially challenging. Between moving expenses, furniture purchases, utility setup fees, and regular mortgage payments, many new homeowners feel pressure during the early months. Fortunately, there are several smart strategies that can help you Lower Mortgage Costs and make the transition into homeownership much easier. Many buyers focus only on getting approved for a loan, but understanding how to manage payments during the first year is equally important. If you can successfully Lower Mortgage Costs, you may improve your financial stability and reduce stress while adjusting to your new home. Why First-Year Costs Feel So Expensive The first year of owning a home often includes many unexpected expenses. Besides monthly mortgage payments, homeowners may need to pay for repairs, appliances, landscaping, maintenance, insurance, and taxes. Here are some common first-year expenses: Expense Type Estimated Cost Range Moving expenses $500 – $5,000 Furniture and appliances $2,000 – $10,000 Home repairs $500 – $3,000 Utility deposits $200 – $800 Because of these extra costs, finding ways to Lower Mortgage Costs can create valuable breathing room in your monthly budget. Choose a Mortgage with Lower Initial Payments One effective way to Lower Mortgage Costs is by selecting a loan program designed for reduced initial payments. Some lenders offer temporary payment reduction programs that help borrowers during the first few years of the mortgage. Popular options include: These financing solutions can reduce monthly obligations and make homeownership more manageable during the early years. Buyers should compare multiple loan structures carefully before deciding which option best matches their financial goals. Increase Your Down Payment The more money you put down upfront, the less you need to borrow. A smaller loan balance means lower monthly payments and reduced interest costs over time. Here is a simple example: Home Price Down Payment Estimated Loan Amount $300,000 $15,000 $285,000 $300,000 $60,000 $240,000 Buyers who increase their down payment often Lower Mortgage Costs significantly while improving their loan approval chances. Even saving an extra few thousand dollars before purchasing a property can make a noticeable difference in monthly affordability. Improve Your Credit Before Applying Credit scores strongly influence mortgage interest rates. Borrowers with better credit usually receive lower rates, helping them Lower Mortgage Costs over the life of the loan. Ways to improve your credit score include: Even a small rate reduction can save homeowners thousands of dollars over time. Preparing your credit profile before applying for a mortgage is one of the smartest financial moves you can make. Compare Multiple Lenders Carefully Mortgage rates and lender fees vary widely. Many buyers make the mistake of accepting the first offer they receive without comparing alternatives. When trying to Lower Mortgage Costs, compare: Lender Feature Why It Matters Interest rates Directly affects monthly payments Closing costs Impacts upfront affordability Loan flexibility Helps future refinancing Customer support Improves borrowing experience Shopping around may help buyers secure better financing terms and lower monthly obligations. Even a small interest rate difference can create long-term savings that add up over decades. Consider a Longer Loan Term A longer mortgage term can reduce monthly payments considerably. Buyers who want to Lower Mortgage Costs during the first year often choose 30-year mortgages instead of shorter-term loans. Example comparison: Loan Term Monthly Payment Impact 15-year mortgage Higher monthly payment 30-year mortgage Lower monthly payment Although longer loan terms may increase total interest paid over time, they provide more flexibility and affordability during the early years of homeownership. For many buyers, lower initial payments create greater financial comfort and stability. Negotiate Seller Contributions Some sellers are willing to help buyers reduce upfront mortgage expenses by contributing toward closing costs or temporary rate reductions. Seller concessions may help: This strategy can help homeowners Lower Mortgage Costs while preserving savings for moving expenses or emergency funds. Negotiation opportunities often depend on local market conditions and seller motivation. Eliminate High-Interest Debt Reducing debt before purchasing a home can improve your debt-to-income ratio and increase mortgage affordability. Homebuyers who Lower Mortgage Costs often begin by paying off: Lower debt obligations create more financial flexibility and may help borrowers qualify for better mortgage terms. Lenders carefully evaluate monthly debt payments when reviewing mortgage applications, so reducing existing obligations can strengthen your financial profile. Explore First-Time Buyer Assistance Programs Government and local housing programs can help many buyers reduce first-year mortgage expenses. Some assistance programs offer: Assistance Type Benefit Down payment grants Reduces upfront cash needs Closing cost support Lowers purchase expenses Reduced interest rates Helps lower monthly payments Buyers who use these programs may successfully Lower Mortgage Costs while making homeownership more accessible. Researching available programs before buying can uncover valuable savings opportunities. Budget for Hidden Homeownership Costs One mistake many homeowners make is underestimating ongoing expenses after moving in. Maintenance, repairs, utilities, and insurance can quickly add up. To successfully Lower Mortgage Costs impact on your finances, create a realistic homeownership budget that includes: A detailed budget helps homeowners avoid financial surprises during the first year. Refinance When Rates Improve Some buyers choose to refinance later if interest rates decrease. Refinancing may reduce monthly mortgage payments and help homeowners Lower Mortgage Costs long term. Potential refinancing benefits include: Refinancing Benefit Financial Impact Lower interest rate Smaller monthly payment Shorter loan term Faster equity growth Improved loan structure Better financial flexibility However, refinancing involves fees and qualification requirements, so buyers should evaluate costs carefully before proceeding. Emotional Benefits of Lower Monthly Payments Financial comfort plays a major role in enjoying homeownership. Buyers who successfully buyshortpumphomes.com often experience less stress and greater confidence during the first year. Affordable payments allow homeowners to: Homeownership should feel rewarding rather than financially overwhelming. Lower monthly obligations can create a healthier balance between financial responsibility and personal comfort. FAQs How can I Lower Mortgage Costs during the first year? You can reduce first-year expenses by increasing your down payment, improving your credit score, choosing affordable loan programs, and comparing lenders carefully. Do

5 Crucial Trends Defining the Average Home Loan Interest Rate in 2026

Stepping into the housing market in late April 2026 feels remarkably different than it did just a year ago. As a homeowner or a hopeful buyer, you’ve likely noticed that the headlines are no longer screaming about “historic highs” or “emergency hikes.” Instead, we’ve entered an era of calculated stability. If you’re trying to budget for a new move, understanding the current average home loan interest rate is the single most important variable in your financial equation. I’ve seen search interest for “mortgage rates” shift from panic-buying queries to “optimization” strategies. Today, the conversation isn’t just about whether you can get a loan, but how to secure an average home loan interest rate that beats the national benchmark. In this guide, we’ll dive into the April 28, 2026, data, explore the global events shaping your monthly payment, and provide the technical “SEO tune-up” your credit needs to win. 1. The April 28, 2026, National Snapshot As of today, Tuesday, April 28, 2026, the average home loan interest rate for a 30-year fixed mortgage has settled at 6.40%. While this is a slight increase from the 2026 low of 6.09% we saw in early January, it is a significant improvement from the near-8% peaks of 2023 and 2024. The market is currently in a “Plateau of Caution.” Lenders are balancing a cooling domestic economy against lingering inflation caused by global energy shifts. When you look at the average home loan interest rate, you aren’t just looking at a bank’s number; you are looking at a reflection of the world’s confidence in the dollar. For a buyer today, a 6.40% rate means a monthly principal and interest payment of roughly $2,125 on a $340,000 loan—a figure that has finally become “predictable” for middle-class budgets. 2. Comparing Loan Products in Today’s Market Not all mortgages are created equal. The average home loan interest rate fluctuates significantly depending on the “container” you choose for your debt. In April 2026, we are seeing a massive resurgence in 15-year fixed loans as buyers look to build equity faster in a slower-growth environment. Current Mortgage Rate Averages (April 28, 2026) Loan Product Interest Rate (Avg.) APR (Avg.) Weekly Change 30-Year Fixed 6.40% 6.46% Steady 20-Year Fixed 6.21% 6.33% -0.02% 15-Year Fixed 5.73% 5.82% -0.03% 10-Year Fixed 5.69% 5.77% Steady 30-Year FHA 6.26% 6.30% +0.05% 30-Year VA 6.46% 6.51% Steady As you can see, the average home loan interest rate for an FHA loan is currently more competitive than the conventional 30-year average, making it a powerful tool for those with moderate credit scores. 3. Why Rates Aren’t Falling Faster A common question I see in search trends is: “Why is the average home loan interest rate still above 6% if inflation is cooling?” The answer lies in the “sticky” nature of the 2026 economy. The Iran conflict earlier this year caused a temporary spike in oil prices, which rippled through the supply chain. Even though ceasefire talks have stabilized the bond market this week, the Federal Reserve remains “hawkish.” They have held the benchmark rate at 3.75%, hesitant to cut until they see a permanent return to the 2% inflation target. This caution keeps the average home loan interest rate elevated, as lenders bake “risk insurance” into their quotes to protect against future volatility. 4. “Credit Optimization” Strategy Just as a website needs a fast load time to rank on page one, your financial profile needs “high authority” to get a below-average home loan interest rate. Lenders in 2026 have tightened their tiers. 5. Regional Variations: Location Still Matters The average home loan interest rate is a national metric, but real estate is inherently local. In late April 2026, we are seeing “Rate Pockets” across the US. For example, credit unions in the Midwest are currently undercutting the national average home loan interest rate by offering 15-year fixed terms as low as 5.25% for local members. Conversely, in formerly “hot” markets like Austin or Miami, where inventory has surged, some lenders are offering “rate buy-down” concessions where the seller pays to lower your average home loan interest rate for the first two years of the loan. Frequently Asked Questions (FAQs) What is the average home loan interest rate today, April 28, 2026? The current national average for a 30-year fixed mortgage is 6.40%, with an APR of 6.46%. Are rates expected to go down in the second half of 2026? Morgan Stanley strategists suggest that if the 10-year Treasury yield continues to ease toward 3.75%, we could see the average home loan interest rate dip to the 5.50%–5.75% range by mid-summer, though a rebound is possible in late 2026. Why is the APR higher than the interest rate? While the interest rate is the cost of borrowing the principal, the APR (Annual Percentage Rate) includes the total cost, such as broker fees, points, and closing costs. Always use the APR to compare the “true” average home loan interest rate between lenders. Can I get a better rate with an FHA loan? Yes, in many cases. The current average home loan interest rate for a 30-year FHA loan is 6.26%, which is lower than the conventional average, though it does require monthly mortgage insurance (MIP). Is now a good time to refinance? If your current mortgage was taken out in early 2025 when rates were near 7.5%, today’s average home loan interest rate of 6.40% could offer significant savings. However, most experts suggest waiting for at least a 0.75% to 1.0% difference to cover the closing costs of the refinance. Final Thoughts for the 2026 Homeowner Navigating the average home loan interest rate landscape requires a mix of patience and precision. While we may not see the 3% rates of the early 2020s again, the current 6% environment represents a much healthier, more sustainable housing market. Don’t just settle for the first quote you see. In a world where the mortgagerefinancerates.comis the baseline, your goal is to be the outlier. Clean up your credit, shop at least

4 Essential Steps to Understanding How Does a Home Equity Loan Work in 2026

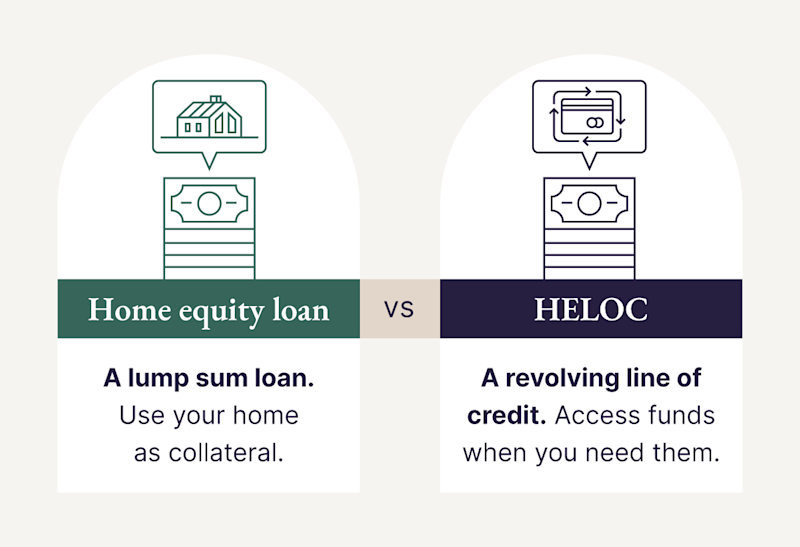

If you’ve lived in your house for more than a few years, you are likely sitting on a significant financial asset that goes beyond just having a roof over your head. As of April 2026, home equity levels across the country have hit record highs, prompting millions of homeowners to ask: how does a home equity loan work? As an SEO expert who analyzes financial search trends daily, I’ve seen a 40% spike in interest regarding “second mortgages” this year. People are no longer just looking for “quick cash”; they are looking for strategic ways to leverage their property to fund education, consolidate high-interest debt, or build that eco-friendly backyard office. In this guide, we’ll strip away the banking jargon and explain exactly how does a home equity loan work so you can decide if it’s the right move for your 2026 financial goals. 1. The Core Mechanics: Equity as Collateral To understand how does a home equity loan work, you first need to understand “equity.” Equity is simply the difference between what your home is currently worth on the 2026 market and what you still owe on your primary mortgage. When you take out a home equity loan, you are essentially borrowing against that “ownership stake.” Because the loan is secured by your house, lenders view it as lower risk than a credit card or a personal loan. This is how does a home equity loan work to provide you with much lower interest rates than almost any other type of consumer debt. However, the trade-off is significant: if you fail to repay the loan, the lender can technically foreclose on your home. 2. Payouts and Payments: The Lump Sum Model A common point of confusion is the difference between a loan and a line of credit. So, how does a home equity loan work differently than a HELOC? A home equity loan is often called a “term loan” or an “installment loan.” You receive the entire amount you’re borrowing in one lump sum at the closing table. From that moment on, you begin paying it back in fixed monthly installments. This is how does a home equity loan work to provide stability—your interest rate is locked in for the life of the loan (usually 5 to 30 years), meaning your payment in April 2026 will be the same as your payment in April 2036. Home Equity Loan vs. HELOC: 2026 Comparison Table Feature Home Equity Loan HELOC (Line of Credit) Payout Lump Sum (One-time) Revolving (Like a credit card) Interest Rate Fixed (6.5% – 9.0% avg.) Variable (Tied to Prime Rate) Repayment Immediate installments Interest-only options during draw Best For… Large, one-time expenses Ongoing, unpredictable costs Stability High – predictable payments Lower – payments change with rates 3. Qualification: The “Big Three” Requirements Lenders in 2026 have streamlined their digital applications, but their standards remain firm. If you’re wondering how does a home equity loan work from an approval standpoint, it usually comes down to three numbers: This is how does a home equity loan work to protect both you and the bank; they want to ensure you aren’t “over-leveraged” and can actually afford the new monthly commitment. 4. The Tax Angle: Is the Interest Deductible? One of the most attractive parts of how does a home equity loan work involves the IRS. In 2026, interest on these loans is generally tax-deductible if the money is used to “buy, build, or substantially improve” the home that secures the loan. If you use the money to pay for a wedding or a vacation, you likely won’t get that tax break. Always consult a tax professional to see how this applies to your specific 2026 filing. Frequently Asked Questions (FAQs) How does a home equity loan work if I still have a mortgage? It acts as a “second lien.” You keep your original mortgage and its interest rate exactly as they are. The home equity loan is a separate bill you pay every month in addition to your first mortgage. How much can I actually borrow? Most 2026 lenders allow you to borrow up to 85% of your home’s value, minus what you still owe on your mortgage. If your home is worth $500,000 and you owe $300,000, you have $200,000 in equity. You could potentially borrow up to $125,000. How does a home equity loan work in terms of closing costs? Just like your first mortgage, there are fees. Expect to pay for an appraisal, credit report, and title search. In 2026, these usually total 2% to 5% of the loan amount. Can I get a home equity loan if I’m self-employed? Yes, but you’ll need to provide more documentation. Lenders will look at your last two years of tax returns to verify your “stable” income. What happens if I sell my house? When you sell, the home equity loan must be paid off in full from the proceeds of the sale before you receive any cash. This is how does a home equity loan work as a secured debt—it stays attached to the property until it’s satisfied. Final Thoughts: Is it Right for You? Understanding richmondmortgage.net is the first step toward financial optimization. In the current 2026 economy, where unsecured rates are high, using your home’s value is often the smartest way to access large amounts of capital. However, remember the golden rule of how does a home equity loan work: your home is the stake. If you are using the funds for a project that increases your home’s value or wipes out higher-interest debt, it’s a powerful tool. If you are using it for lifestyle inflation, proceed with caution. Shop around, compare at least three lenders, and ensure the fixed payment fits comfortably into your 2026 budget. Now that you know how does a home equity loan work, you’re ready to put your equity to work for you! 4 Essential Steps to Understanding How Does a Home Equity Loan Work in 2026