Veterans, active-duty service members, and eligible military families have a unique opportunity to secure homeownership through a VA mortgage loan. This specialized loan program offers favorable terms, including no down payment, competitive interest rates, and flexibility that other loan programs rarely provide. However, applying for a VA mortgage loan can seem overwhelming if you’re unfamiliar with the process. This guide will walk you through each step in detail, helping you approach your home purchase confidently.

Understanding the VA Mortgage Loan

Before diving into the application process, it’s essential to understand what a VA mortgage loan is and why it matters. The VA mortgage loan is a benefit provided by the U.S. Department of Veterans Affairs to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. Unlike conventional loans, VA mortgage loans often:

- Require no down payment

- Avoid private mortgage insurance (PMI)

- Offer lower interest rates

- Include options for refinancing

| Feature | VA Mortgage Loan | Conventional Loan | FHA Loan |

|---|---|---|---|

| Down Payment | None | Typically 5–20% | 3.5% |

| PMI | None | Required | Required |

| Interest Rate | Competitive | Higher | Moderate |

| Eligibility | Military & veterans | Anyone with credit | Low to moderate income |

| Funding Fee | Required (exempt for disabled vets) | N/A | N/A |

By understanding these differences, it becomes clear why applying for a VA mortgage loan is a valuable step for eligible borrowers.

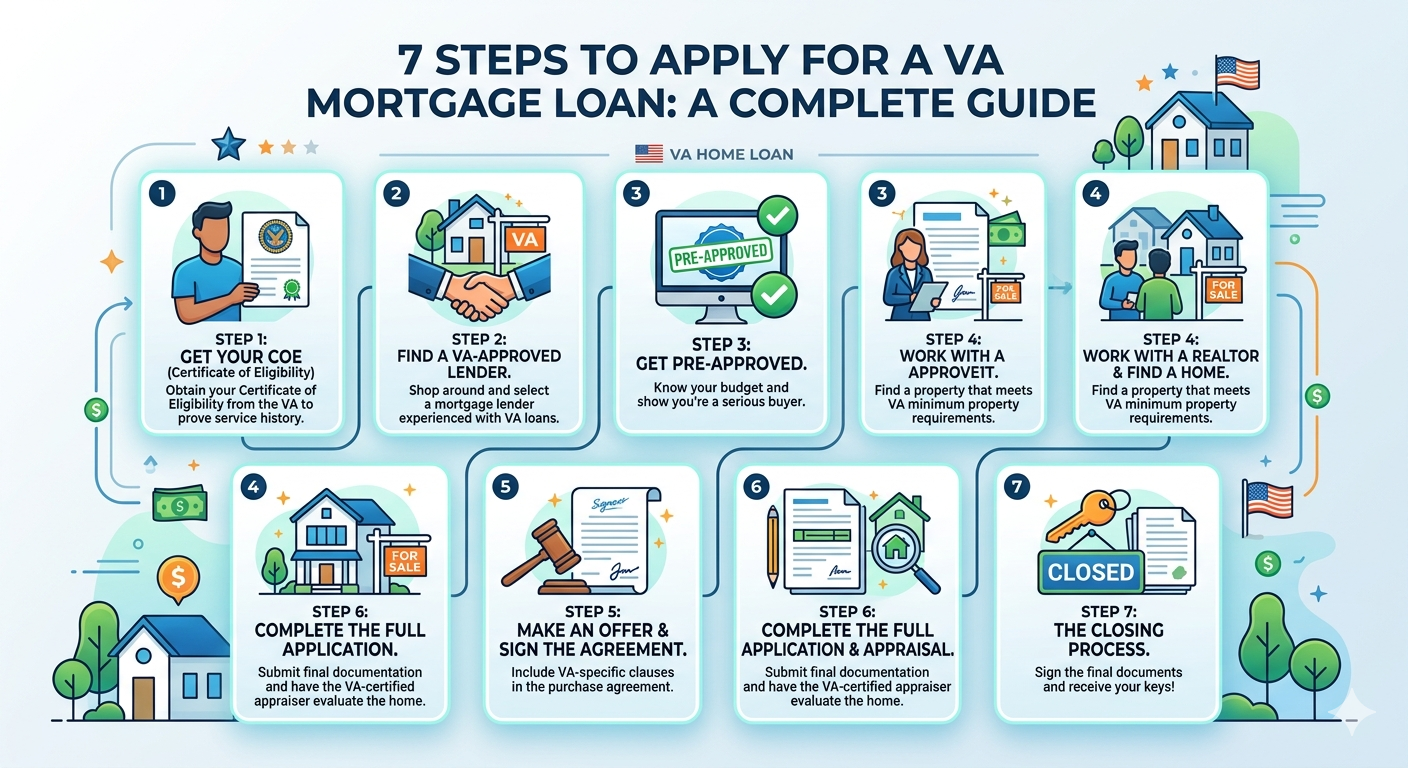

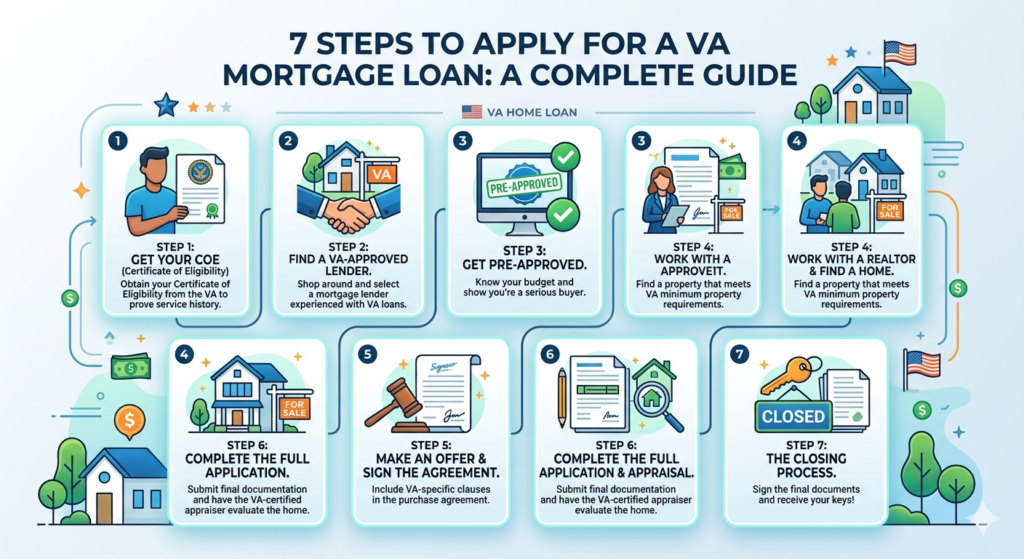

Step 1: Check Your Eligibility

The first step in applying for a VA mortgage loan is determining eligibility. The VA requires that applicants meet one of the following criteria:

- Served 90 consecutive days of active service during wartime

- Served 181 days of active service during peacetime

- Have more than six years of service in the National Guard or Reserves

- Be the surviving spouse of a veteran who died in service or from a service-connected disability

Keep documentation ready, such as your DD Form 214 or other proof of service, as this will be critical when completing your application.

Step 2: Obtain a Certificate of Eligibility (COE)

The Certificate of Eligibility (COE) proves to lenders that you qualify for a VA mortgage loan. You can request your COE through:

- VA eBenefits portal – Online submission is fastest

- Through your lender – Many VA-approved lenders can obtain it for you

- Mail – Submit VA Form 26-1880 to the VA

A COE typically contains your service history, eligibility status, and entitlement. Lenders require this document before approving a VA mortgage loan.

Step 3: Assess Your Financial Readiness

Even though VA mortgage loans offer favorable terms, lenders still assess financial readiness. Important factors include:

- Credit score: While VA loans have more flexible requirements, a higher score improves your chances of a lower interest rate.

- Debt-to-income ratio (DTI): Ideally under 41%, though exceptions exist.

- Income verification: W-2s, pay stubs, or tax returns help lenders evaluate repayment capacity.

| Factor | Recommended Benchmark |

|---|---|

| Credit Score | 620+ (higher preferred) |

| Debt-to-Income | ≤41% |

| Employment History | 2+ years stable employment |

| Savings | Cover closing costs & emergencies |

Preparing your finances ensures a smoother VA mortgage loan application process.

Step 4: Choose a VA-Approved Lender

Not every financial institution can issue VA mortgage loans. Select a VA-approved lender experienced in VA loan processing. Tips include:

- Compare interest rates and fees

- Ask about VA funding fee options

- Ensure the lender understands VA property requirements

Veterans often find that working with a lender familiar with VA loans speeds up approval and reduces stress.

Step 5: Prequalify for a VA Mortgage Loan

Prequalification provides a snapshot of how much home you can afford and demonstrates your seriousness to sellers. The process generally requires:

- COE

- Credit score and financial documents

- Estimated income and debts

After prequalification, your lender will give an estimated loan amount. This is not final approval but a valuable step toward a VA mortgage loan.

Step 6: Submit Your Application

Once prequalified, you can formally apply for your VA mortgage loan. The application (typically Uniform Residential Loan Application – Form 1003) will include:

- Personal information (name, SSN, contact info)

- Employment and income history

- Asset and liability details

- Property information (address, type, purchase price)

Submit your COE, financial documents, and any other lender-specific forms. The lender will then review your application to determine VA mortgage loan eligibility.

Step 7: Underwriting and Approval

After submission, the underwriting team assesses:

- Creditworthiness

- Debt-to-income ratio

- Property appraisal

- VA compliance

The VA requires a Certificate of Reasonable Value (CRV), which ensures the home’s price aligns with its market value. Once approved, your VA mortgage loan moves to closing.

Additional Tips for a Successful VA Mortgage Loan Application

- Understand the VA funding fee – Ranges from 2.15% to 3.3% for first-time users, waived for disabled veterans.

- Check property eligibility – VA loans apply to primary residences only.

- Work with a knowledgeable realtor – They can navigate VA property requirements.

- Avoid new debts – Large purchases during application can affect approval.

- Be prepared for appraisal – VA appraisers focus on safety and market value.

VA Mortgage Loan Refinance Options

VA loans also provide refinance opportunities:

| Refinance Type | Purpose | Benefits |

|---|---|---|

| Interest Rate Reduction Refinance Loan (IRRRL) | Lower interest rate | Simplified process, minimal paperwork |

| VA Cash-Out Refinance | Access home equity | Can pay off debt, renovate, or invest |

Knowing your options ensures you maximize your VA mortgage loan benefits.

Common FAQs About VA Mortgage Loan

Q1: Can I use a VA mortgage loan more than once?

Yes, eligible veterans can use a VA mortgage loan multiple times, as long as entitlement is available.

Q2: Do I need a down payment?

No, VA mortgage loans typically require no down payment, though optional contributions can reduce the funding fee.

Q3: What is the VA funding fee?

It’s a one-time fee paid to the VA to support the program. Amount varies based on service and down payment.

Q4: Can I buy a second home with a VA loan?

No, VA loans are intended for primary residences only.

Q5: How long does VA loan approval take?

From application to closing, approval usually takes 30–45 days, depending on documentation and appraisal speed.

Q6: Can I refinance my existing VA loan?

Yes, through the IRRRL or VA cash-out refinance programs.

Q7: Are VA loans available for condos?

Yes, but the condo must be VA-approved.

Q8: What credit score do I need?

Generally 620+, though lenders may approve lower scores based on compensating factors.

Q9: Do I need homeowners insurance?

Yes, VA loans require standard insurance coverage.

Q10: Can surviving spouses use VA loans?

Yes, under certain conditions, surviving spouses may be eligible.

Conclusion

Applying for a VA mortgage loan can be a smooth and rewarding process when approached with preparation and knowledge. By understanding eligibility, obtaining your COE, working with a VA-approved lender, and staying financially ready, veterans and military families can achieve the dream of homeownership with confidence. Remember, the VA mortgage loan is not just a benefit—it’s a stepping stone to long-term financial stability and security.