If you’ve lived in your house for more than a few years, you are likely sitting on a significant financial asset that goes beyond just having a roof over your head. As of April 2026, home equity levels across the country have hit record highs, prompting millions of homeowners to ask: how does a home equity loan work?

As an SEO expert who analyzes financial search trends daily, I’ve seen a 40% spike in interest regarding “second mortgages” this year. People are no longer just looking for “quick cash”; they are looking for strategic ways to leverage their property to fund education, consolidate high-interest debt, or build that eco-friendly backyard office. In this guide, we’ll strip away the banking jargon and explain exactly how does a home equity loan work so you can decide if it’s the right move for your 2026 financial goals.

1. The Core Mechanics: Equity as Collateral

To understand how does a home equity loan work, you first need to understand “equity.” Equity is simply the difference between what your home is currently worth on the 2026 market and what you still owe on your primary mortgage.

When you take out a home equity loan, you are essentially borrowing against that “ownership stake.” Because the loan is secured by your house, lenders view it as lower risk than a credit card or a personal loan. This is how does a home equity loan work to provide you with much lower interest rates than almost any other type of consumer debt. However, the trade-off is significant: if you fail to repay the loan, the lender can technically foreclose on your home.

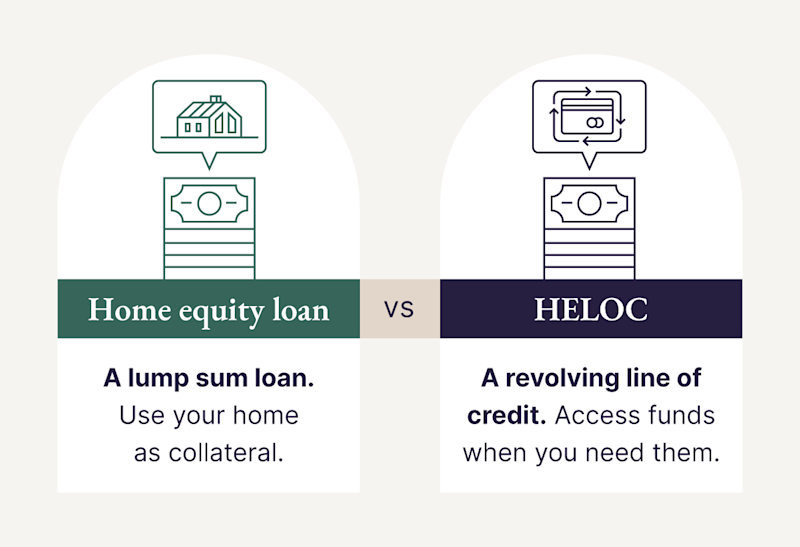

2. Payouts and Payments: The Lump Sum Model

A common point of confusion is the difference between a loan and a line of credit. So, how does a home equity loan work differently than a HELOC?

A home equity loan is often called a “term loan” or an “installment loan.” You receive the entire amount you’re borrowing in one lump sum at the closing table. From that moment on, you begin paying it back in fixed monthly installments. This is how does a home equity loan work to provide stability—your interest rate is locked in for the life of the loan (usually 5 to 30 years), meaning your payment in April 2026 will be the same as your payment in April 2036.

Home Equity Loan vs. HELOC: 2026 Comparison Table

| Feature | Home Equity Loan | HELOC (Line of Credit) |

| Payout | Lump Sum (One-time) | Revolving (Like a credit card) |

| Interest Rate | Fixed (6.5% – 9.0% avg.) | Variable (Tied to Prime Rate) |

| Repayment | Immediate installments | Interest-only options during draw |

| Best For… | Large, one-time expenses | Ongoing, unpredictable costs |

| Stability | High – predictable payments | Lower – payments change with rates |

3. Qualification: The “Big Three” Requirements

Lenders in 2026 have streamlined their digital applications, but their standards remain firm. If you’re wondering how does a home equity loan work from an approval standpoint, it usually comes down to three numbers:

- Credit Score: Most 2026 lenders require a score of 620 to 680. However, to get the absolute best rates, you’ll want a score of 740 or higher.

- CLTV (Combined Loan-to-Value): Lenders generally don’t want your total debt (mortgage + equity loan) to exceed 80% to 85% of your home’s value.

- DTI (Debt-to-Income): Your total monthly debt payments should be less than 43% of your gross monthly income.

This is how does a home equity loan work to protect both you and the bank; they want to ensure you aren’t “over-leveraged” and can actually afford the new monthly commitment.

4. The Tax Angle: Is the Interest Deductible?

One of the most attractive parts of how does a home equity loan work involves the IRS. In 2026, interest on these loans is generally tax-deductible if the money is used to “buy, build, or substantially improve” the home that secures the loan. If you use the money to pay for a wedding or a vacation, you likely won’t get that tax break. Always consult a tax professional to see how this applies to your specific 2026 filing.

Frequently Asked Questions (FAQs)

How does a home equity loan work if I still have a mortgage?

It acts as a “second lien.” You keep your original mortgage and its interest rate exactly as they are. The home equity loan is a separate bill you pay every month in addition to your first mortgage.

How much can I actually borrow?

Most 2026 lenders allow you to borrow up to 85% of your home’s value, minus what you still owe on your mortgage. If your home is worth $500,000 and you owe $300,000, you have $200,000 in equity. You could potentially borrow up to $125,000.

How does a home equity loan work in terms of closing costs?

Just like your first mortgage, there are fees. Expect to pay for an appraisal, credit report, and title search. In 2026, these usually total 2% to 5% of the loan amount.

Can I get a home equity loan if I’m self-employed?

Yes, but you’ll need to provide more documentation. Lenders will look at your last two years of tax returns to verify your “stable” income.

What happens if I sell my house?

When you sell, the home equity loan must be paid off in full from the proceeds of the sale before you receive any cash. This is how does a home equity loan work as a secured debt—it stays attached to the property until it’s satisfied.

Final Thoughts: Is it Right for You?

Understanding richmondmortgage.net is the first step toward financial optimization. In the current 2026 economy, where unsecured rates are high, using your home’s value is often the smartest way to access large amounts of capital.

However, remember the golden rule of how does a home equity loan work: your home is the stake. If you are using the funds for a project that increases your home’s value or wipes out higher-interest debt, it’s a powerful tool. If you are using it for lifestyle inflation, proceed with caution. Shop around, compare at least three lenders, and ensure the fixed payment fits comfortably into your 2026 budget. Now that you know how does a home equity loan work, you’re ready to put your equity to work for you!

4 Essential Steps to Understanding How Does a Home Equity Loan Work in 2026