Veterans and active military members have access to one of the most powerful home financing tools available: the VA mortgage loan. These loans, guaranteed by the U.S. Department of Veterans Affairs, provide unique benefits compared to conventional mortgages. If you’ve ever wondered, “what is a VA mortgage loan?” this article will give you a complete, humanized guide while ensuring it’s optimized for search engines.

In this guide, we’ll explore everything from eligibility and benefits to interest rates and frequently asked questions. By the end, you’ll have a comprehensive understanding of why a VA mortgage loan can be a game-changer for military families.

What Is a VA Mortgage Loan?

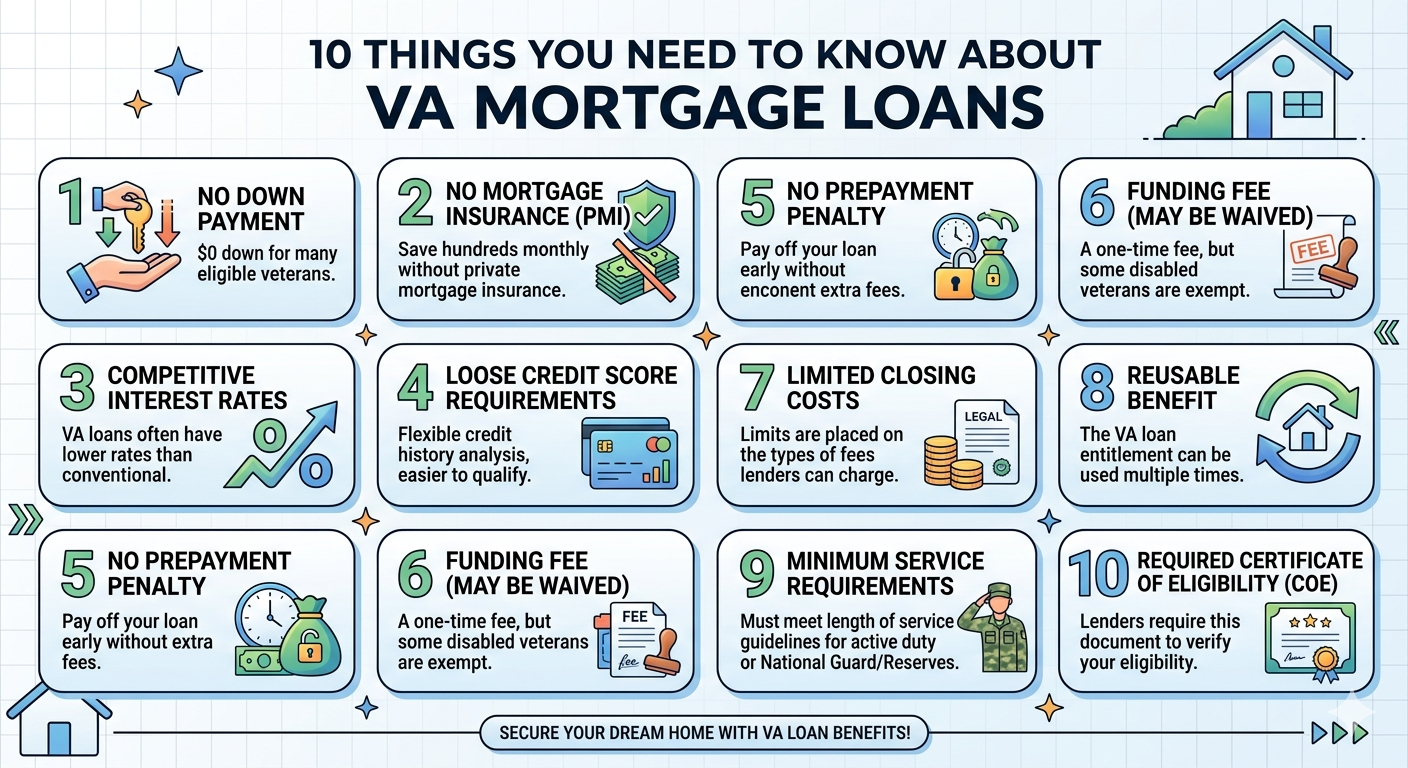

A VA mortgage loan is a home loan specifically designed for veterans, active-duty service members, and certain surviving spouses. Unlike conventional loans, a VA mortgage loan is partially guaranteed by the Department of Veterans Affairs, reducing risk for lenders.

Key points:

- No down payment required in most cases

- Competitive interest rates

- No private mortgage insurance (PMI)

- Flexible credit requirements

Essentially, a VA mortgage loan makes homeownership more accessible and affordable for those who have served the country.

1. VA Mortgage Loan Eligibility

Not everyone qualifies for a VA mortgage loan. Eligibility is primarily based on military service. Here’s a simplified table outlining who can apply:

| Service Type | Minimum Service Requirement |

|---|---|

| Active-duty service members | 90 consecutive days during wartime |

| Active-duty service members | 181 days during peacetime |

| Veterans | 90 days of active service during wartime |

| Veterans | 181 days of active service during peacetime |

| National Guard / Reserves | 6 years of service or 90 days of active duty |

| Surviving spouse | Spouse of veteran who died in service |

It’s important to note that eligibility can vary depending on the period of service and other factors, but a VA mortgage loan is generally available to anyone meeting these criteria.

2. Key Benefits of a VA Mortgage Loan

A VA mortgage loan comes with benefits that make it a highly attractive option compared to conventional loans. These include:

- No down payment – Unlike conventional loans that require 3%–20%, VA loans often require no down payment.

- No PMI – Borrowers save money because VA loans don’t require private mortgage insurance.

- Competitive interest rates – VA loans often have lower interest rates than conventional or FHA loans.

- Flexible credit guidelines – Veterans with less-than-perfect credit can still qualify.

- Funding fee options – While a VA funding fee is typical, it can be rolled into the loan or waived for certain veterans.

3. VA Mortgage Loan Funding Fee

A unique feature of the VA mortgage loan is the funding fee. This fee helps maintain the program’s sustainability.

| Veteran Type | Funding Fee Percentage (First-time use) |

|---|---|

| Regular military, no down payment | 2.15% |

| Regular military, 5% down payment | 1.50% |

| Reserve / National Guard, no down payment | 2.40% |

| Disabled veterans | 0% |

The funding fee can usually be financed into the total loan amount, which reduces the upfront burden for veterans.

4. VA Mortgage Loan Limits

While a VA mortgage loan doesn’t require a down payment, there are limits to how much you can borrow without one.

| County Loan Limit (2026) | Max Loan Without Down Payment |

|---|---|

| Standard counties | $726,200 |

| High-cost counties | Up to $1,089,300 |

These limits may change yearly and depend on the county in which the home is located. Knowing your county’s limit helps plan your VA mortgage loan strategy effectively.

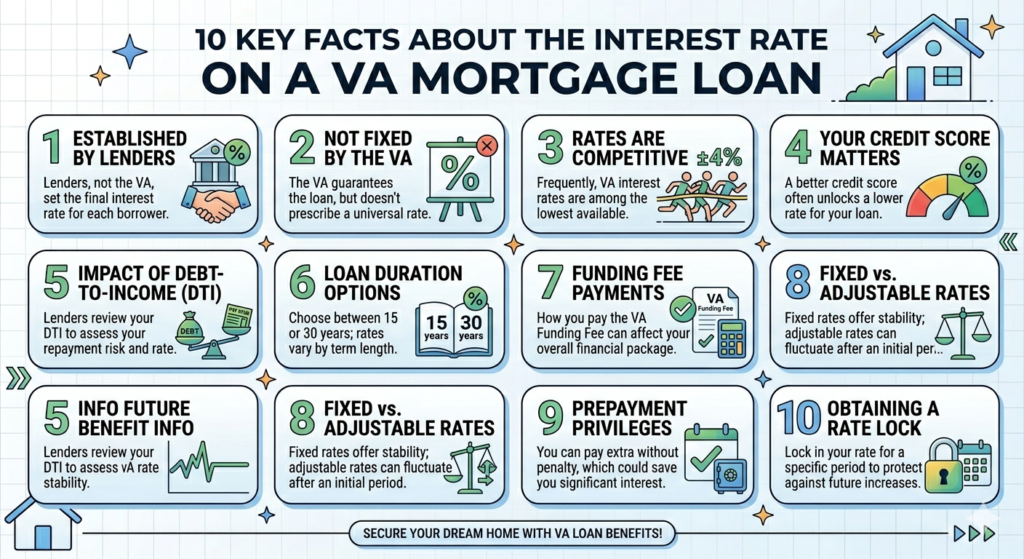

5. VA Mortgage Loan Interest Rates

Interest rates for a VA mortgage loan are generally lower than conventional or FHA loans. Typical rates for 30-year fixed VA loans in 2026 range from 5.5% to 6%, depending on credit score, location, and lender.

| Loan Type | Typical VA Interest Rate | Typical Conventional Rate |

|---|---|---|

| 30-year fixed | 5.75% | 6.25% |

| 15-year fixed | 5.00% | 5.50% |

| Adjustable-rate (5/1) | 5.25% | 5.75% |

Lower rates mean more affordability for veterans, especially when combined with the no PMI requirement.

6. VA Mortgage Loan Application Process

Applying for a VA mortgage loan involves several steps:

- Obtain a Certificate of Eligibility (COE) – This document proves to lenders that you’re eligible for a VA mortgage loan.

- Choose a lender – Not all lenders offer VA loans, so select one experienced with the program.

- Pre-approval – Submit financial information to receive a pre-approval letter.

- Home appraisal – VA requires a home appraisal to ensure fair value and safety.

- Underwriting & closing – Once approved, sign documents and fund your VA mortgage loan.

7. VA Mortgage Loan Refinance Options

Veterans can also refinance existing loans using the VA program:

- Interest Rate Reduction Refinance Loan (IRRRL) – Also called a VA streamline refinance, this helps reduce your interest rate and monthly payment.

- Cash-out refinance – Allows you to take out cash from your home equity, paying off your current mortgage and receiving extra funds.

Both options are designed to maximize the affordability and flexibility of a VA mortgage loan.

8. VA Mortgage Loan vs Conventional Loan

Here’s how a VA mortgage loan compares to conventional loans:

| Feature | VA Loan | Conventional Loan |

|---|---|---|

| Down payment | 0% in most cases | 3–20% |

| PMI | Not required | Required if <20% down |

| Funding fee | Yes, can be financed | None |

| Credit flexibility | More flexible | Stricter requirements |

| Interest rate | Often lower | Often higher |

Veterans save money upfront and monthly with a VA mortgage loan, making homeownership far more accessible.

9. Common Misconceptions About VA Mortgage Loans

Despite its benefits, many veterans are unaware of the VA mortgage loan program’s details. Common myths include:

- “You must have perfect credit.” – VA loans are flexible, and even those with credit challenges can qualify.

- “Only active-duty members are eligible.” – Veterans and certain surviving spouses also qualify.

- “VA loans are complicated.” – While documentation is required, the process is straightforward and lender-supported.

Understanding the facts can help veterans confidently pursue a VA mortgage loan.

10. Tips for Maximizing Your VA Mortgage Loan

To make the most of a VA mortgage loan:

- Shop multiple lenders for the best interest rate

- Maintain stable employment and clean credit records

- Consider the funding fee when planning your budget

- Keep an eye on county loan limits

- Use refinance options strategically to reduce interest or cash out equity

Following these tips ensures your VA mortgage loan remains both affordable and advantageous.

FAQs About VA Mortgage Loans

Q1: Can I use a VA mortgage loan more than once?

A1: Yes, veterans can use the VA mortgage loan multiple times, but funding fees may apply based on previous use.

Q2: Do I need a down payment for a VA mortgage loan?

A2: In most cases, no. However, loans exceeding county limits may require a down payment.

Q3: Can I finance the funding fee?

A3: Yes, the VA funding fee can usually be rolled into your total loan amount.

Q4: How long does it take to close a VA mortgage loan?

A4: Closing typically takes 30–45 days, depending on lender and appraisal timing.

Q5: Can surviving spouses qualify for a VA mortgage loan?

A5: Yes, spouses of veterans who died in service or from service-connected causes may be eligible.

Q6: Are VA loans assumable?

A6: Yes, VA loans can be transferred to another qualified veteran, which can be a selling advantage.

Q7: Can I use a VA mortgage loan to buy a second home?

A7: No, VA loans are intended for primary residences only.