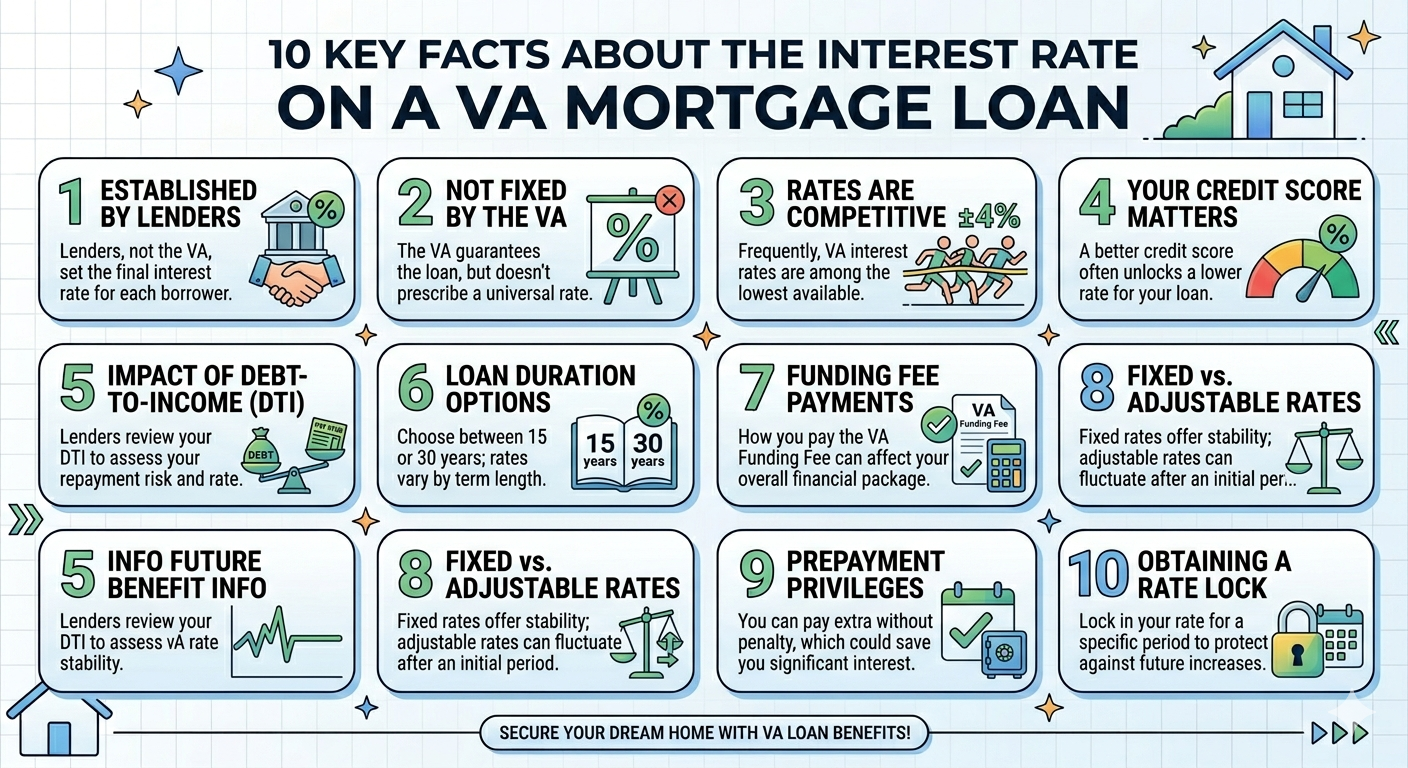

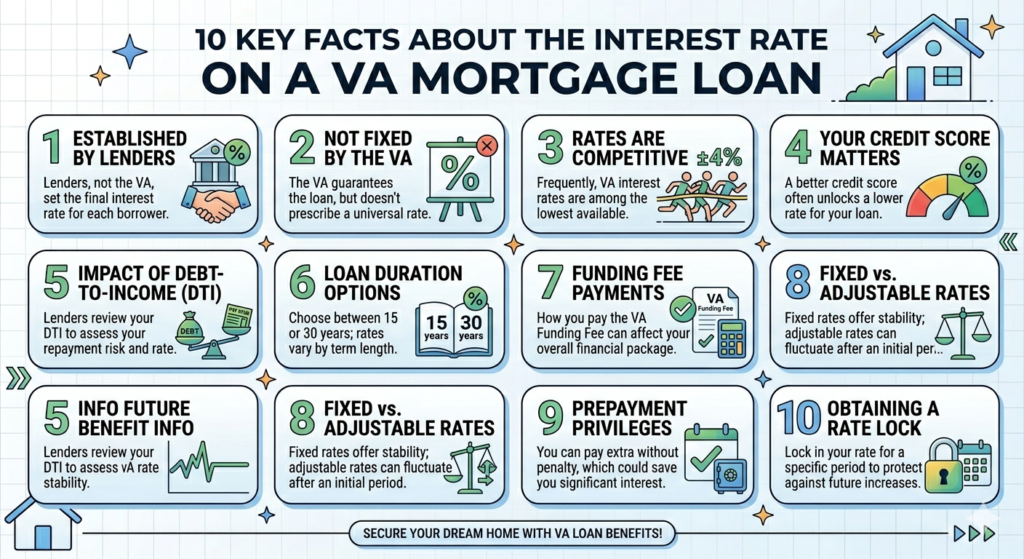

The interest rate on a VA mortgage loan is one of the most crucial factors for veterans, active-duty service members, and eligible surviving spouses considering homeownership. Understanding how VA loans work, what affects the interest rate, and how it compares to other loan types can save borrowers thousands of dollars over the life of a mortgage. This guide explores everything you need to know about VA loan interest rates in a detailed, natural, and easy-to-understand way.

What Is a VA Mortgage Loan?

A VA mortgage loan is a home loan guaranteed by the U.S. Department of Veterans Affairs (VA). Unlike conventional loans, VA loans are designed specifically to support veterans, service members, and eligible surviving spouses in buying a home with favorable terms. One of the key advantages of a VA loan is that it often provides lower interest rates and minimal upfront costs compared to conventional mortgages.

The interest rate on a VA mortgage loan can vary depending on the borrower’s credit, loan size, and lender policies. Generally, VA loans offer competitive rates that are often lower than those of conventional loans, helping borrowers save money over time.

How Is the Interest Rate on a VA Mortgage Loan Determined?

Several factors influence the interest rate on a VA mortgage loan, including:

| Factor | Explanation |

|---|---|

| Credit Score | Borrowers with higher credit scores usually receive lower interest rates. |

| Loan Term | 15-year vs. 30-year loan terms can affect the rate; shorter terms often have lower rates. |

| Loan Amount | Jumbo loans may have slightly higher interest rates than standard VA loan limits. |

| Market Conditions | Current economic factors, inflation, and mortgage market trends can impact rates. |

| Lender Policies | Different VA-approved lenders may offer varying rates based on their cost structures. |

By understanding these factors, borrowers can make informed decisions and potentially secure a lower interest rate on a VA mortgage loan.

Average VA Loan Interest Rates in 2026

Interest rates fluctuate regularly due to market conditions. As of early 2026, the average interest rate on a VA mortgage loan for a 30-year fixed-rate loan ranges from 5.5% to 6.2%, while 15-year VA loans average 4.8% to 5.3%.

| Loan Type | Average Interest Rate |

|---|---|

| 30-Year Fixed VA Loan | 5.5% – 6.2% |

| 15-Year Fixed VA Loan | 4.8% – 5.3% |

| Adjustable-Rate VA Loan (5/1 ARM) | 5.1% – 5.7% |

These rates are indicative, and individual circumstances such as credit profile, lender offers, and loan size can influence the final rate.

VA Loan vs. Conventional Loan Interest Rates

Veterans often choose VA loans because of lower rates and fewer fees. Here’s a comparison:

| Loan Type | Typical Interest Rate | Benefits |

|---|---|---|

| VA Loan | 5.5% – 6.2% | No down payment, no private mortgage insurance (PMI), competitive rates |

| Conventional Loan | 6.0% – 6.8% | Requires 5-20% down payment, PMI required if down payment <20% |

Notice that the interest rate on a VA mortgage loan is generally lower, which can translate into significant savings over the loan term.

Factors That Can Lower Your VA Loan Interest Rate

There are strategies to reduce your interest rate on a VA mortgage loan, including:

- Improving Credit Score – Higher credit scores typically qualify for lower rates.

- Making a Down Payment – Optional down payments may reduce the interest rate slightly.

- Shopping Around – Different VA-approved lenders offer different rates.

- Shorter Loan Terms – Choosing a 15-year term may result in a lower interest rate.

- Reducing Debt-to-Income Ratio (DTI) – Lenders may offer lower rates to borrowers with lower DTI.

Applying these strategies can help veterans maximize the benefits of a VA loan.

Fixed vs. Adjustable VA Loan Interest Rates

VA loans offer both fixed and adjustable rates. Understanding the differences is essential:

| Loan Type | Description | Pros | Cons |

|---|---|---|---|

| Fixed-Rate | Interest rate remains constant for the loan term | Predictable monthly payments, easy budgeting | Slightly higher initial rates compared to ARM |

| Adjustable-Rate (ARM) | Rate adjusts after a set period, e.g., 5/1 ARM | Lower initial rate, potential savings if rates drop | Risk of rate increase, monthly payment can rise |

Borrowers seeking stability often choose fixed-rate loans, while those confident in future income or planning to move may prefer adjustable-rate VA loans.

The Role of VA Funding Fee in Interest Rates

VA loans do not require private mortgage insurance (PMI), but most borrowers pay a VA funding fee. This fee does not directly affect the interest rate on a VA mortgage loan, but it can influence the total loan amount.

| Military Category | Funding Fee (No Down Payment) |

|---|---|

| First-time use | 2.15% |

| Subsequent use | 3.3% |

| Veterans with disability | Waived |

Some lenders may offer slightly better rates to borrowers who make an optional down payment or pay the funding fee upfront.

Refinancing a VA Loan: Interest Rate Benefits

Veterans can refinance to lower their interest rate on a VA mortgage loan using:

- Interest Rate Reduction Refinance Loan (IRRRL) – Streamlines refinancing to reduce interest rates with minimal paperwork.

- Cash-Out Refinance – Borrowers can access equity but may have slightly higher rates than IRRRL.

Refinancing to a lower interest rate can reduce monthly payments and overall interest paid across the loan term.

Common Misconceptions About VA Loan Interest Rates

- VA Loans Always Have the Lowest Rates – While VA loans are competitive, some conventional or FHA loans may occasionally have lower rates.

- Funding Fee Increases Interest Rate – The VA funding fee is added to the loan, not directly to the interest rate.

- All Lenders Offer Same Rate – Lenders set their rates individually, even for VA loans.

- Credit Score Doesn’t Matter – Credit still affects the rate and loan approval process.

Understanding these points ensures veterans avoid surprises when applying for a VA mortgage.

Benefits of Low VA Loan Interest Rates

Lower interest rates on a VA mortgage loan provide multiple advantages:

- Reduced Monthly Payments – Easier to budget for housing costs.

- Long-Term Savings – Lower total interest over 15-30 years.

- Increased Buying Power – More affordable loans mean buyers can consider higher-value homes.

- Financial Security – Predictable payments reduce stress and risk.

How to Compare VA Loan Interest Rates

When comparing VA loans, consider:

| Comparison Factor | Why It Matters |

|---|---|

| APR vs. Interest Rate | APR includes fees, giving a better total cost picture |

| Loan Term | 15-year vs 30-year affects monthly payments and total interest |

| Lender Fees | Origination, closing costs, and other fees can influence effective rates |

| Credit Requirements | Lenders may offer lower rates to higher credit scores |

By comparing these factors, veterans can secure the most favorable interest rate on a VA mortgage loan.

Tips to Secure the Best VA Loan Rate

- Check Your Credit Report – Address errors and improve scores.

- Get Pre-Approved – Strengthens negotiating power with lenders.

- Consider Rate Lock – Locking a rate can protect against market increases.

- Explore Multiple Lenders – Rates vary across VA-approved lenders.

- Consider Shorter Loan Terms – Often lower interest rates and faster payoff.

Following these tips can help maximize the savings from your VA loan.

FAQs About VA Mortgage Loan Interest Rates

Q1: What is the current interest rate on a VA mortgage loan?

A: Current rates vary, but for a 30-year fixed VA loan, they generally range from 5.5% to 6.2% as of 2026.

Q2: Can I get a lower rate if I make a down payment?

A: Yes, while VA loans do not require a down payment, making one may slightly lower your interest rate.

Q3: Are VA loan rates always lower than conventional loans?

A: Typically, yes, but market fluctuations can occasionally make conventional loans competitive.

Q4: How does my credit score affect the VA loan interest rate?

A: Higher credit scores usually qualify for lower interest rates, while lower scores may result in slightly higher rates.

Q5: Can I refinance my VA loan to a lower rate?

A: Yes, VA offers Interest Rate Reduction Refinance Loans (IRRRL) to help borrowers reduce their interest rate.

Q6: Does the VA funding fee increase my interest rate?

A: No, the funding fee is added to the loan amount, not the interest rate.

Q7: What’s the difference between fixed and adjustable VA loan rates?

A: Fixed rates stay constant, offering predictability, while adjustable rates may change after an initial period.

Q8: How can I shop for the best VA loan rate?

A: Compare multiple VA-approved lenders, check APRs, fees, and loan terms before committing.

Q9: Does loan term affect the VA interest rate?

A: Yes, shorter loan terms often have lower interest rates but higher monthly payments.

Q10: Are VA loan rates negotiable?

A: Yes, borrowers can sometimes negotiate lender fees or interest rate discounts based on creditworthiness.

Conclusion

Understanding the interest rate on a VA mortgage loan is essential for veterans and service members seeking homeownership. These rates are generally lower than conventional loans and, combined with benefits like no down payment and no PMI, make VA loans a powerful tool for achieving the dream of owning a home. By comparing lenders, considering loan terms, and improving credit, borrowers can secure a rate that maximizes savings and affordability.

Whether you are buying your first home, upgrading, or refinancing, paying attention to the interest rate on a VA mortgage loan ensures financial stability and long-term success in homeownership.